The situation in the Middle East is ever-changing.

Investors are constantly monitoring the newsflow coming out of the U.S. and Iran, and most importantly, Trump’s X account.

Risks are high, and things are uncertain.

That’s where consumer stocks shine. They are still in demand regardless of the state of the global economy.

In this article, we will detail three consumer stocks in Singapore and Hong Kong that are undervalued and delivering big dividends.

Investment Thesis and Catalyst

Slow and steady.

The Middle East conflict could cause a recession if global crude oil and natural gas prices remain high for the rest of the year.

Consumer stocks have traditionally been resistant to recessions and risks, and investors shift their money to them when things go bad.

They are also great dividend companies, as they consistently pay out a high share of their earnings in dividends.

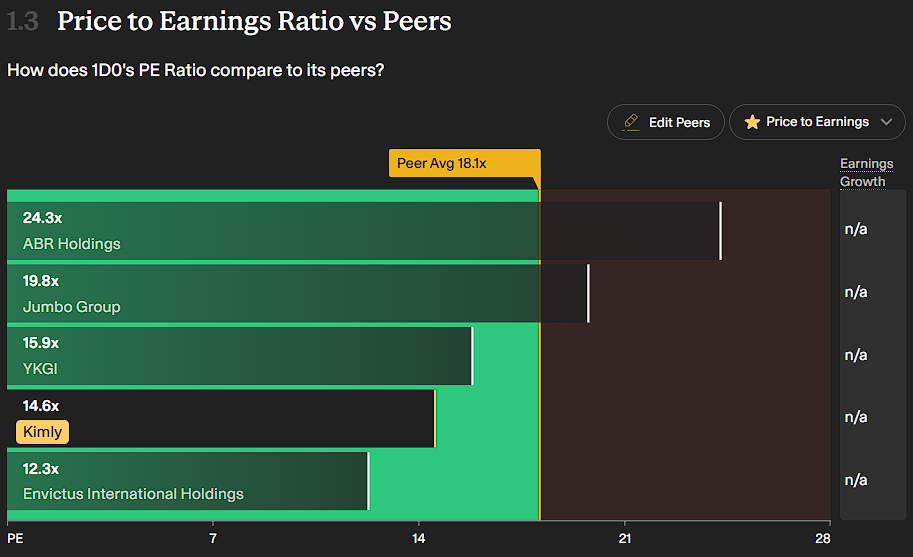

Kimly (Singapore)

Kimly manages and operates food outlets or coffee shops under the Kimly, foodclique, and Kedai Kopi brands. It also has restaurants under the Tonkichi and Tenderfresh brands.

It is listed on the Singapore Exchange and has a market capitalisation of SG$491 million.

Kimly’s valuation is relatively cheap now. It is trading at a price-to-earnings (PER) ratio of 14.6 times compared to its peers’ average of 18.1 times.

Source: SimplyWallSt

Furthermore, its dividend yield is also high at 5.1%, averaging the same from 2021 to 2025. And it has increased its dividend payout ratio from 42% in 2021 to 75% in 2025.

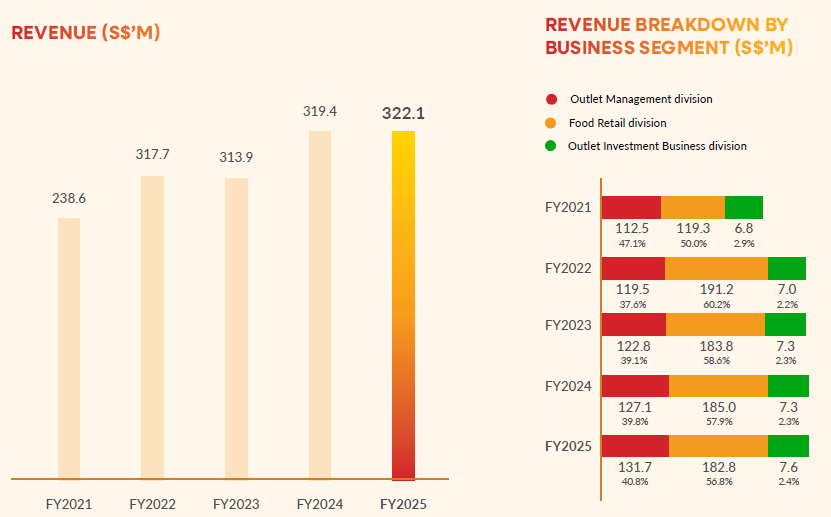

Kimly’s financial growth in the past five years has been strong. Revenue grew at an average annual growth rate of 7.8% from 2021 to 2025. However, its profits have also declined since 2021, due to higher selling, general, and administrative expenses.

- Its food retail division remains its most profitable segment with a profit margin of 19%, compared to its outlet management (10.5%) and outlet investment (16.6%).

- The food retail division contributes the most to revenue at 57%.

Source: Kimly Annual Report 2025

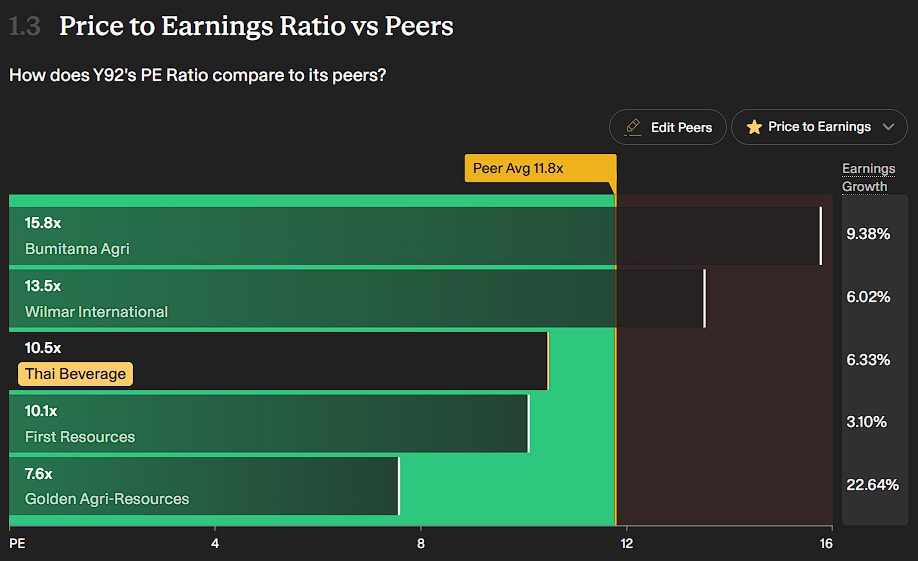

Thai Beverage (Singapore)

Thai Beverage (ThaiBev) is a Thai beverage company that is listed on the Singapore Exchange and sells four main product types – spirits, beer, non-alcoholic beverages and food – in Southeast Asia.

It is currently worth SG$10.6 billion in market capitalisation.

ThaiBev is trading at low valuations, with a PER of 10.5 times compared to its peers’ average of 11.8 times. Meanwhile, it is also below its 5-year historical average of 13.3 times.

Source: SimplyWallSt

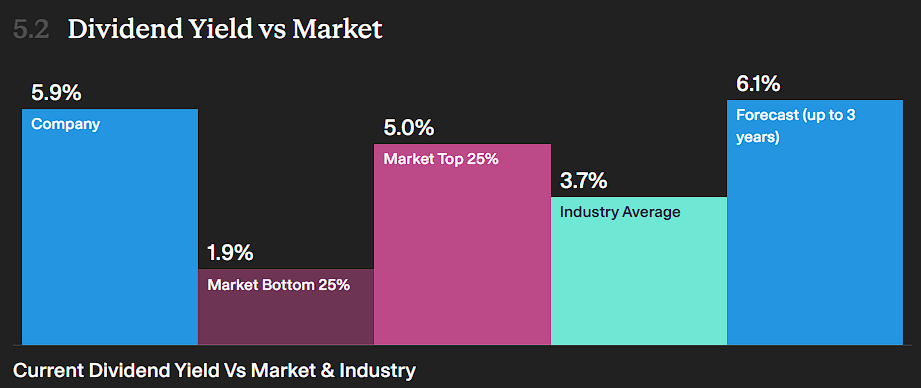

Let’s look at its dividend track record.

- The dividend yield is high at 5.9% currently, compared to 3.7% of the industry average.

- It has also been steadily increasing its dividend payout ratio from 53.9% in 2024 to 61.4% in 2025.

Source: SimplyWallSt

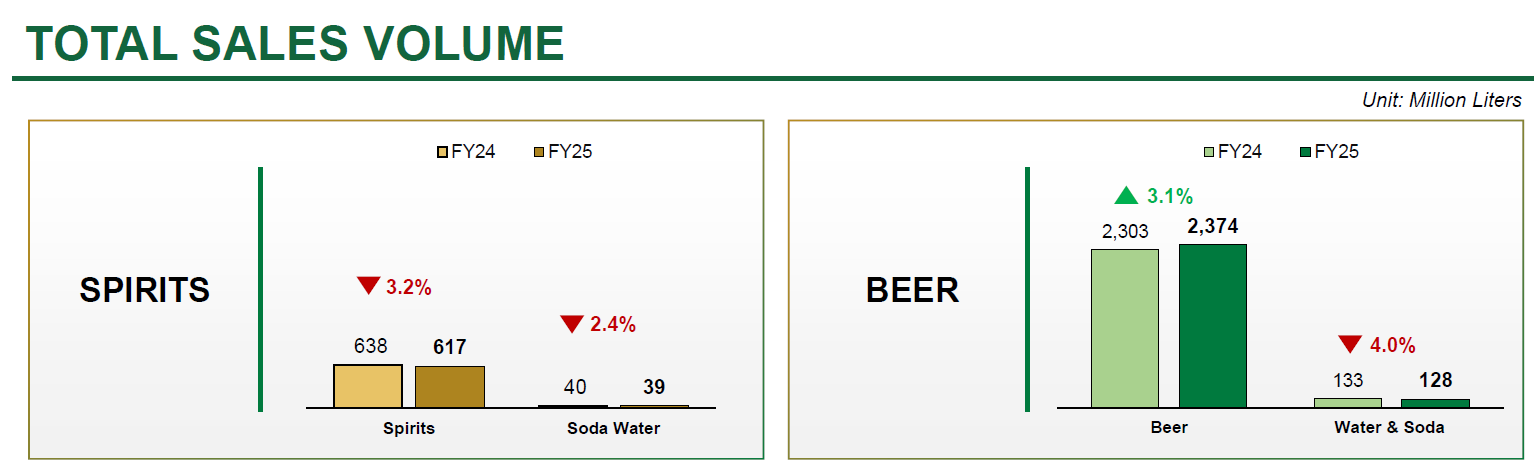

2025 is a normalisation year for ThaiBev. Revenue declined slightly by 2.1% to SG$333 million in 2025 from SG$340 million in 2024, driven mainly by lower sales in spirits. Beer makes up the majority of its business with 37% of revenue, followed by spirits (36%), non-alcoholic beverages (19%).

Source: ThaiBev FY 25 Results Presentation

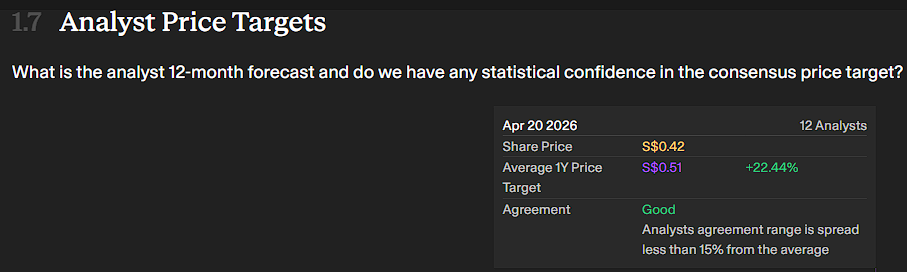

However, analysts in the market are projecting that ThaiBev could have some upside potential. The average target price is set at SG$0.51 with an implied upside of +22.4%.

Source: SimplyWallSt

Bosideng International (Hong Kong)

Bosideng International operates and sells down apparel brands in China, such as Bosideng, Snow Flying, Binjora, and others.

It is listed on the Hong Kong Exchange and currently has a market capitalisation of HKD48 billion.

Bosideng is trading at a PER of 12.1 times, slightly lower than its peers’ average of 12.4 times, but much cheaper compared to its 5-year historical average of 16.1 times.

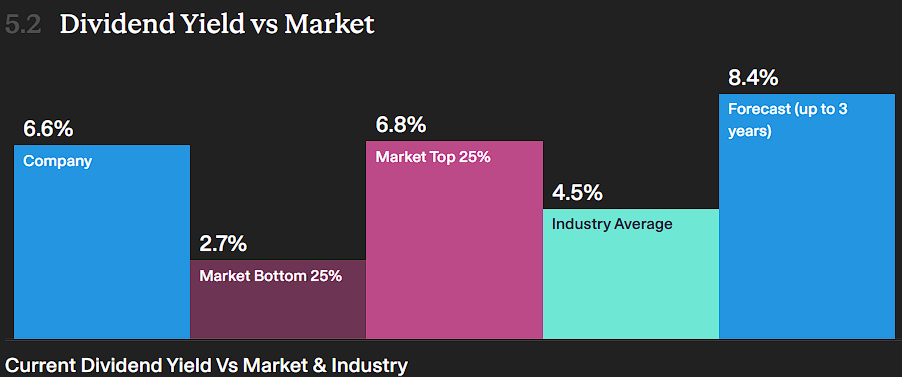

Meanwhile, it also generates a high dividend of 6.6%, higher than the industry average of 4.5%. The dividend payout ratio is also high at about 84%.

Source: SimplyWallSt

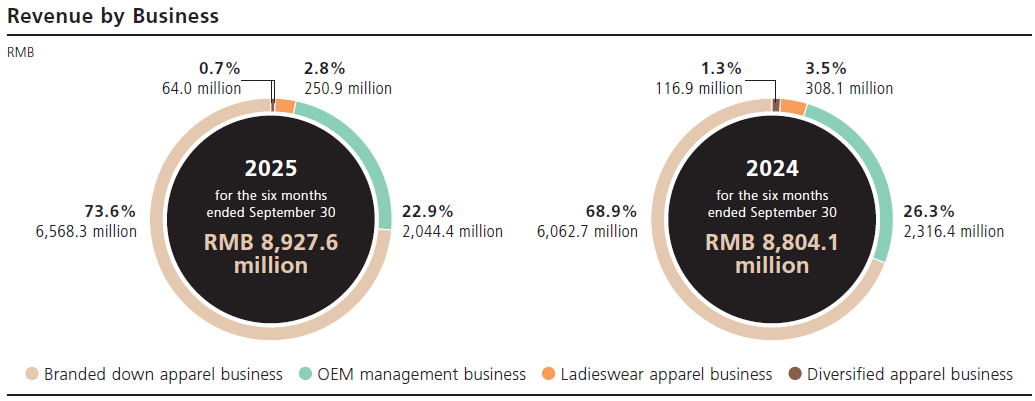

Bosideng remains anchored by its core business of down apparel, where it contributed nearly three-quarters of its revenue in 1H 2025 (Mar-Sep 2025).

- Revenue for 1H 2025 is up slightly by 1.4% to RMB8.9 billion, driven mainly by its down apparel business (+8.3%).

- However, its other segments declined, especially OEM management (-11.7%) and ladieswear (-18.6%).

In China, the sales of clothes and apparel are picking up very strongly in 2026. Retail sales of clothes, shoes, hats, and textiles rose to 9.3% for the months between January and March 2026, compared to 2025’s annual growth rate of 3.2%.

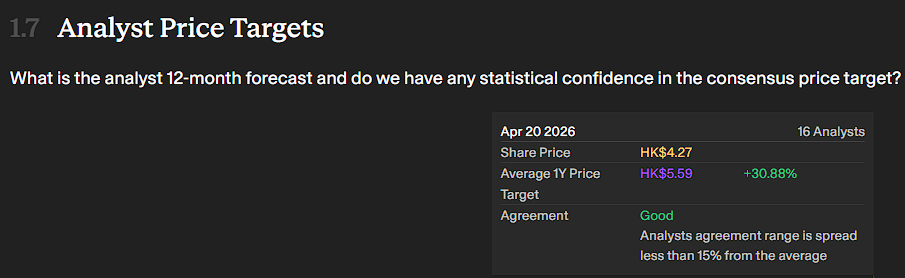

Analysts in the market are high on the stock. The average target price is set at HK$5.59 with an implied upside of +30.9%.

Conclusion

As the world gets more uncertain by the day and the risks of a global recession increase, the consumer sector could prove to be the go-to for investors looking for safety and stability.

It’s best to look for undervalued opportunities with high potential upside and high dividend yields to shield against volatile markets.

Join our newsletter and unlock access to hidden gems and top dividend stocks and REITs: https://www.smallcapasia.com/#subscribe.