Shipping is one of the most risky industries.

But it also comes with great rewards. The conflict between the U.S. and Iran has caused a bottleneck in one of the most important trading routes, the Strait of Hormuz.

Hence, ships are in short supply, and existing ships are seeing a lot of demand. Less supply, higher price. Higher price, higher revenue and profits.

Here are 3 shipping companies that could gain from higher freight and transportation rates.

Investment Thesis and Catalyst

Shipping companies are risky because they require high initial capital. They need a lot of money to buy ships, and it takes a long time to construct.

They also need to comply with a lot of regulations around the world. The industry spends a lot of money protecting its ships, as they go through waters where pirates could hijack them.

But companies that are able to navigate these challenges could benefit when freight rates rise. This is especially true during periods of supply disruption or route congestion. According to Trading Economics, the Containerized Freight Index, which tracks weekly spot rates for shipping containers from Shanghai to major global ports, was up 18.29% over the past month and 39.85% year over year as of May 28, 2026.

Source: Trading Economics

COSCO Shipping (Hong Kong)

COSCO Shipping Holdings (COSCO) transports goods through ships from one port to another across the world.

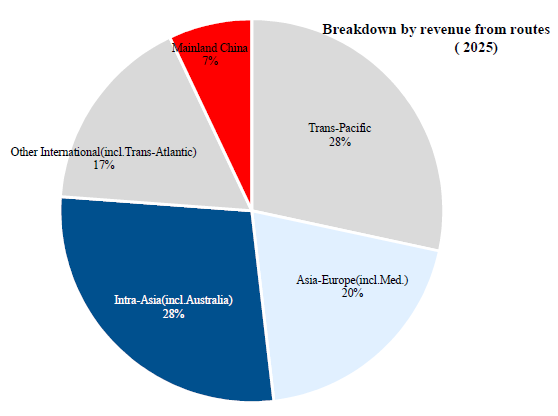

Most of its shipping lines are within Asia (including Australia), which contributes 28% of its revenue in 2025. This is followed by trans-Pacific (28%, from Asia to the Americas), Asia to Europe (20%), other international routes (17%), and finally within mainland China (7%).

Source: COSCO 2025 Annual Presentation

COSCO could be on the cusp of a strong quarter in 2Q 2026. International freight rates are now increasing, and the company has a high exposure in the Pacific, European and Mediterranean routes (about 48% of revenue in 2025).

Its financial performance has followed the flow of freight price fluctuations.

When the supply of freight was tight during the pandemic, revenue more than doubled in 2021 and grew by 13.1% in 2022. In 2023, when economies reopened fully, revenue crashed by more than half. In 2024, revenue recovered by 33.5% while declining by 6.1% in 2025.

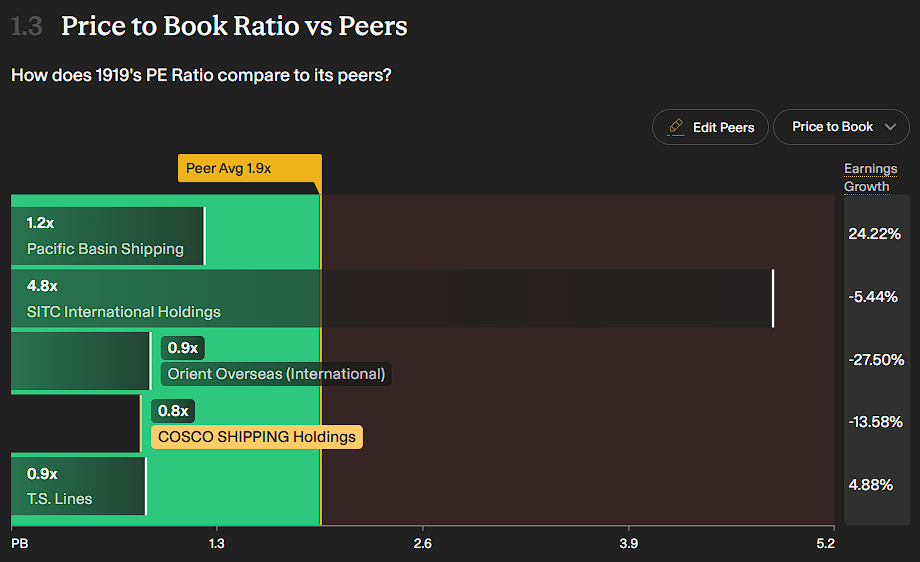

COSCO is currently trading at a price-to-book ratio of 0.8 times, lower than its peers’ average of 1.9 times.

Source: SimplyWallSt

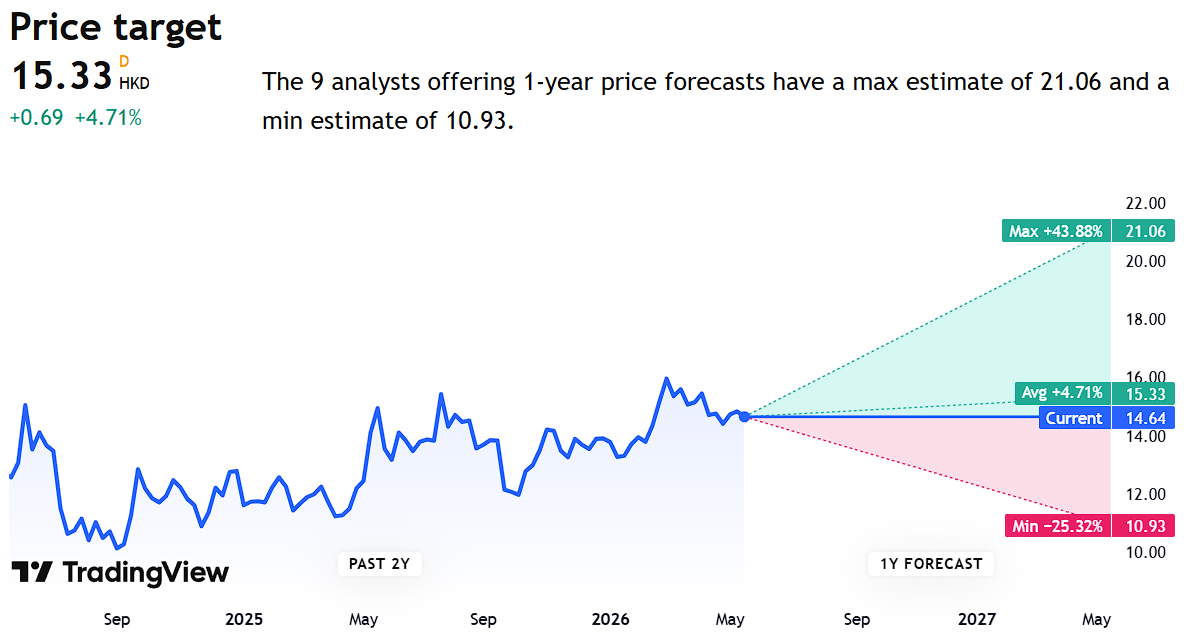

It currently has a high dividend yield of 7.8%, making it an attractive dividend play. Analysts in the market are targeting a price of HK$15.3, with an implied upside of about +4.7%.

Source: TradingView

MTT Shipping & Logistics (Malaysia)

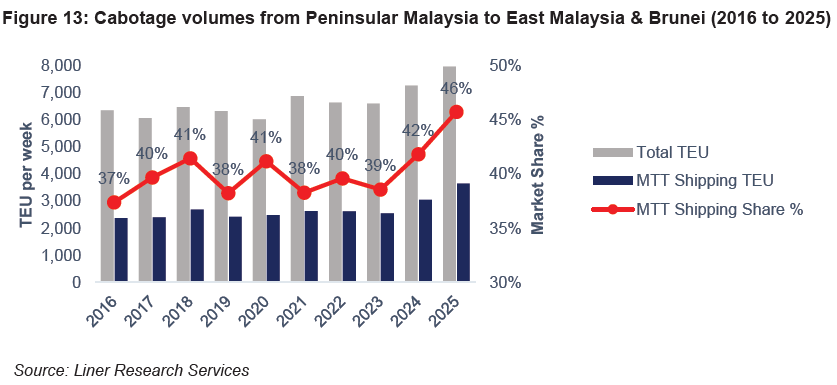

MTT Shipping and Logistics (MTT) transports containers on ships mainly through its Malaysian routes. It is currently the market leader in the routes between West Malaysia and East Malaysia with a 46% market share.

Source: MTT Prospectus

MTT has just been listed on the Malaysian market. And it is currently trading below its offer price of MY$1.03 as investors fear the impact of high fuel costs on shipping companies. However, with its dominant market position on its Malaysian routes, it can pass on costs to its clients.

From 2023 to 2025, revenue grew steadily at an average annual rate of 6.9%, while profits grew at a rate of 2.5%.

According to its prospectus, there is still a supply shortage in the overall shipping segment, especially smaller-sized ones. This will provide pricing support for MTT’s shipping freight and charter rates.

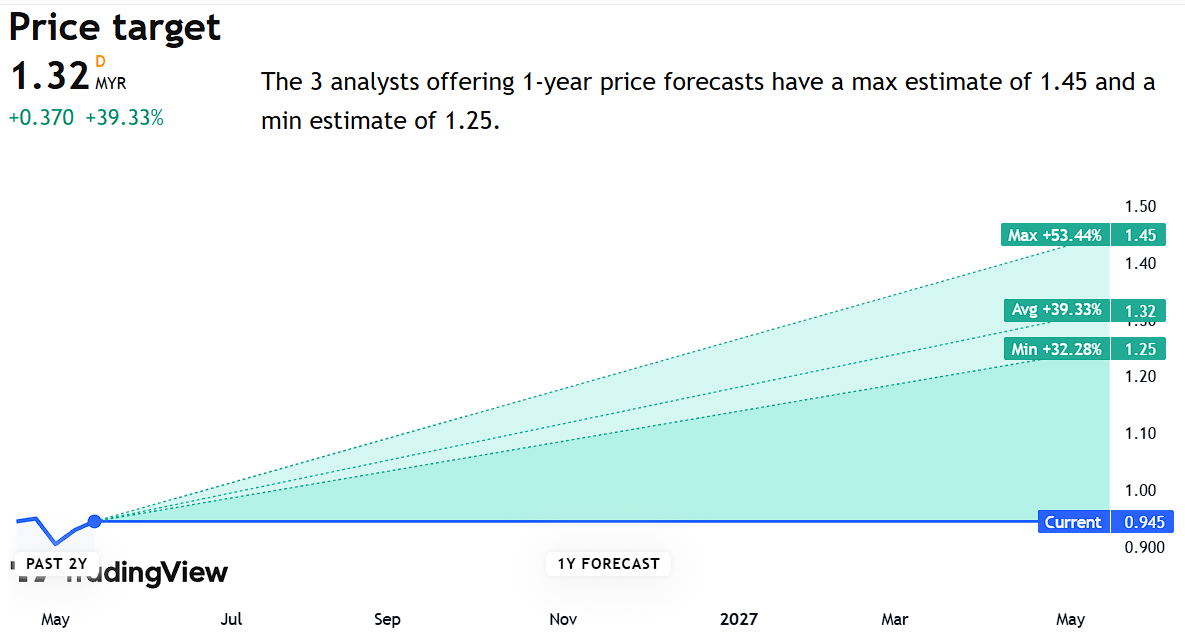

Market analysts are bullish on MTT, setting an average target price of MY$1.32 and an implied upside of +39.3%.

Source: TradingView

Orient Overseas International (Hong Kong)

Orient Overseas (Orient) provides container transport and logistics services. Most of its revenue is derived from within Asia (including Australia) and trans-Pacific routes, making up about 71% in 2025.

Orient is positioned quite strongly for 2026. But let’s look at context first.

Like COSCO, Orient’s fortunes are tied to freight rates and also the global trading environment. In 2025, revenue declined by 9.2% as companies were hesitant to ship products amid Trump tariffs that rattled markets.

- Its trans-Pacific route declined by 17% as a result. America’s West Coast route revenue declined by 22%, while its East Coast route was down by 17%.

However, some Trump-era tariffs have faced legal challenges and policy reversals. Reuters reported that U.S. Customs and Border Protection would stop collecting tariffs imposed under the International Emergency Economic Powers Act after a Supreme Court ruling, while noting that other tariffs, including Section 232 and Section 301 measures, remained unaffected. This may help reduce some uncertainty around selected trade routes, though the broader tariff environment remains fluid.

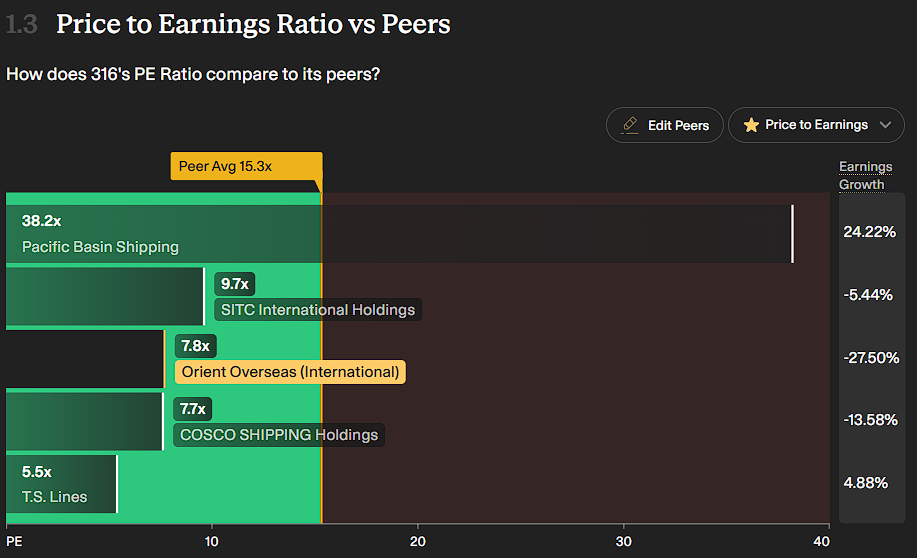

Orient is currently trading at a strong dividend yield of 6.3%. Valuation is attractive with a price-to-earnings ratio of 7.8 times compared to its peers’ average of 15.3 times.

Source: SimplyWallSt

Meanwhile, market analysts think there is still some gas left in the tank. The average target price is set at HK$142 with an implied upside of about +2%.

Source: TradingView

Conclusion

Geopolitical conflicts are hard to predict. But the conflict is causing freight rates to increase and presents an opportunity for investors looking to ride global trends.

Take a good look at your portfolio and see how these shipping companies fit within it.

Join our newsletter and unlock access to hidden gems and top dividend stocks and REITs: https://www.smallcapasia.com/#subscribe.