REITs are a great asset class for income-seeking investors. The requirement to pay out at least 90% of their earnings as distributions makes them perfect for investors who look for a steady, dependable payout.

The recent surge in in the 10 year US treasury yield led to the decline of REITs share prices and resulting in an overall rise in distribution yields for the REIT sector.

Investors are worried about whether REITs can manage the higher borrowing costs given that REITs are highly leveraged. We highlight 3 REITs with distribution yields of 7% and above and determine if they could be good bargains and still be able to give out consistent DPU.

First Real Estate Investment Trust

I first mentioned First Real Estate Investment Trust (First REIT) in this article. I wrote then First REIT could outperform the REIT index. this year.

Though it has underperformed the REIT index as the share price fell 5.56% year to date as at 10 Dec 2023 compared to the REIT index which fall by 5.41%, it still manage to outperform the so called better REITs such as Mapletree Pan Asia commercial Trust which fell by 14.97% based on 10 Dec 2023 price and Lendlease REIT which fell by 12.68%. It even outperform its peer Parkway Life REIT which dipped by 5.84%!

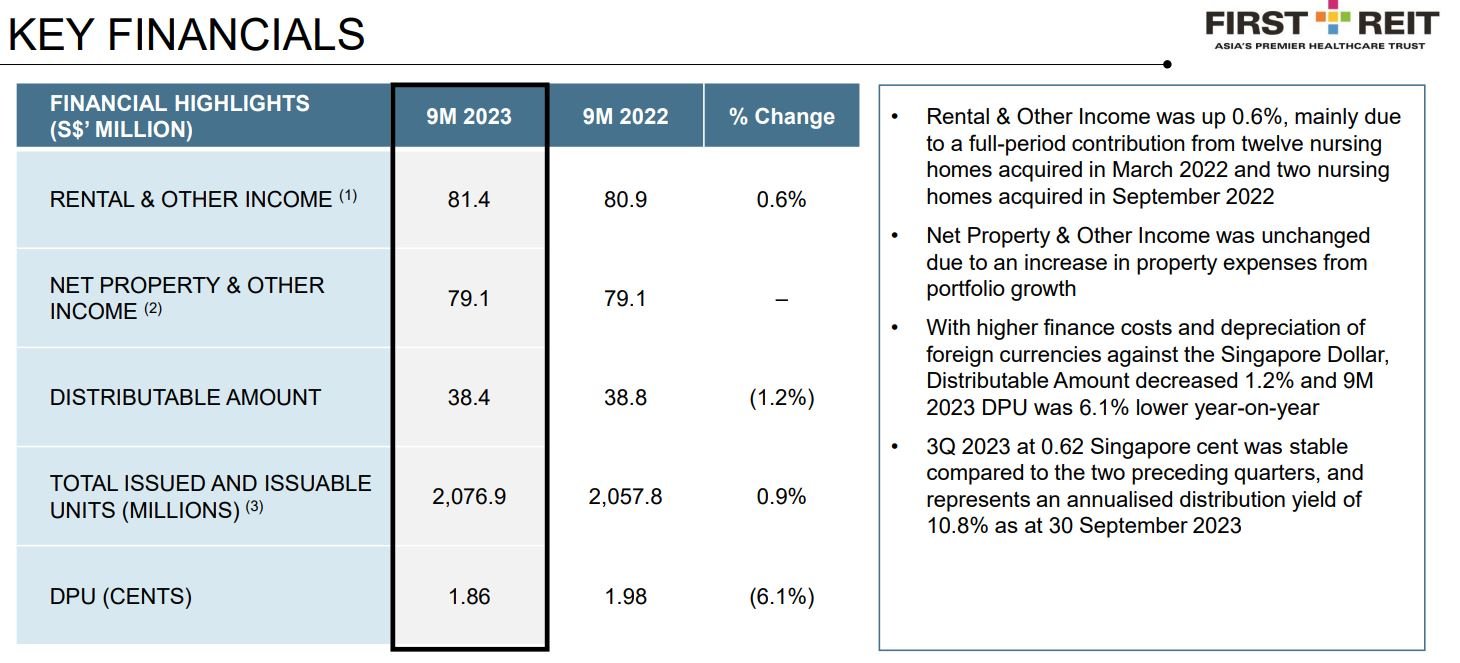

In its 9M 2023 results, DPU dropped 6.1% to 1.86 cents. 3Q 2023 DPU however is stable at 0.62 cents. This translate to an annualised yield of 9.7%! Net property income is unchanged at S$79.1 million. Gearing ratio is still relatively comfortable at 39%.

For its debt maturity profile, First REIT has no refinancing requirements until May 2026. This will put First REIT in a comfortable position if interest rates remain high.

In addition, First REIT is looking to divest Imperial Aryaduta Hotel & Country Club which is a non core asset. This will reduce First REIT gearing further which is especially important in times of high interest rates.

You can view the REIT website here.

Sabana Industrial Real Estate Investment Trust

Sabana Industrial REIT is one of the most underrated REIT. May investors shun this REIT as it does not have a strong sponsor, poor track record in the past and now the removal of the external manager to be replaced by a internal manager.

Despite all these negative news on Sabana REIT, its share price dropped by just 5.81% slightly underperform the REIT index. However, it outperform many investors favourite REIT, CapitaLand Integrated Commercial Trust which has seen its share price dropped by 6.4%!

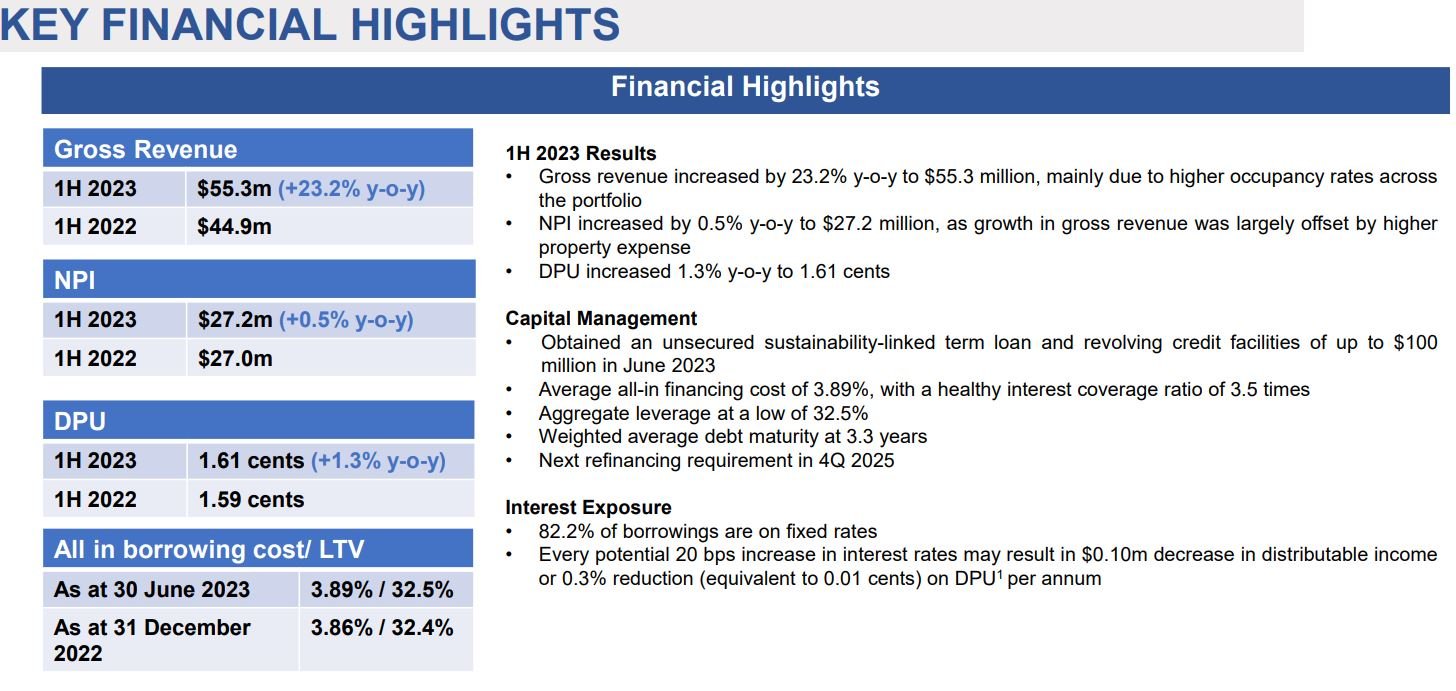

For the first half 2023, net property income increased by 0.5% to S$27.2 million. Portfolio occupancy reach a new high of 93.9%. Gearing ratio is still low at 32.5% and the next financing requirement is only due 4Q2025.

This will enable the REIT to be well prepared should interest rates remain high year. REITs that is due for refinancing next year will face higher borrowing costs and thus impact DPU

DPU increase by 1.3% to 1.61 cents which translates to annualized yield of 8.0%! In addition, the REIT does not make reckless acquisitions just to grow AUM and enhance management fees unlike other REITs which will destroy shareholder value.

You can view the REIT website here.

Lendlease Global Commercial REIT

Many investors and bloggers like Lendlease Global Commercial REIT (LL REIT). Its share price has fallen 12.68% year to date and is looks attractive at current valuation. However, is it worth a buy now?

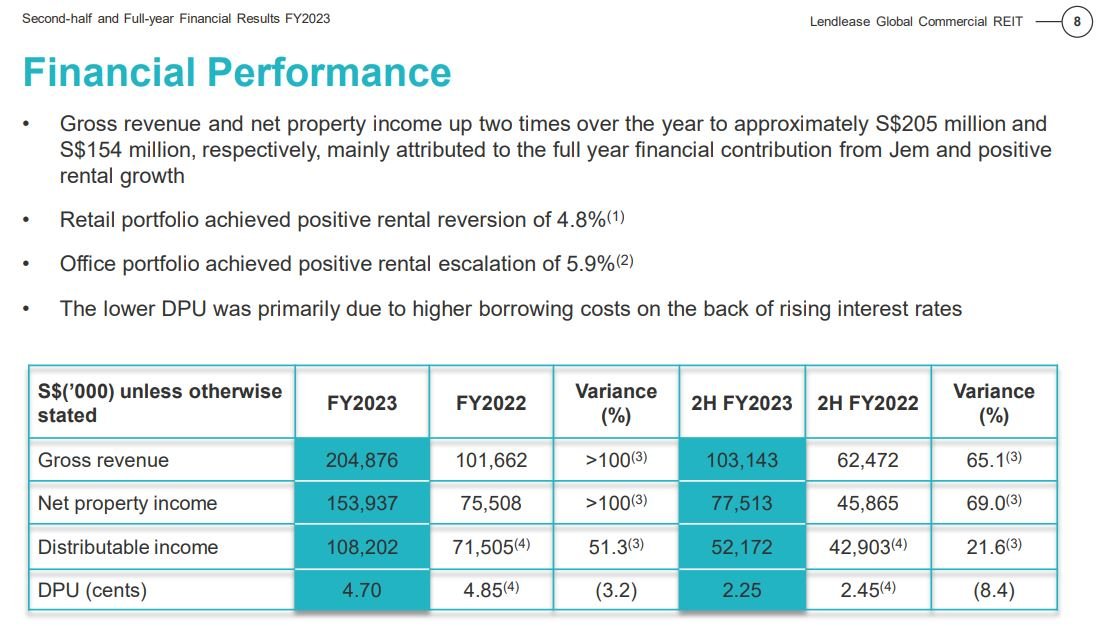

For FY2023, net property income increase by more than 100% due to the contribution from acquisition of JEM. However, DPU dropped by 3.2% to 4.7 cents which translate to dividend yield of more than 7.6%!

Gearing ratio is relatively high at 40.6%. With the recent acquisition of 10% stake in Parkway Parade, it will further increase its gearing ratio. In times of low interest rates, acquisition of assets to grow its DPU is a very logical move.

However, when interest rates are high, investors have to question whether any acquisitions of assets will really increase its DPU. For example the acquisition of JEM just increase its property income and AUM, but did we see an increase in DPU?

This clearly reflects in its share price with Mr Market punish the share price by dropping 12.68% year to date.

You can view the REIT website here.

Conclusion

These are the 3 REITs with distribution yields of 7% or more. However, investors should not be entice by high yield REITs. More importantly when REITs make any acquisitions, investors should question themselves whether is it really true it is DPU accretive as what the REIT manager will usually claim.

In addition, we also should ask ourselves does the acquisition is just to increase AUM and management fees at the expense of shareholders as in the case of LL REIT?

To avoid investing in losing money S-REITs, join our latest Dividend Kaki membership as we show you a fuss-free way to invest in dividend stocks and REITs. Many people love dividend investing, but few truly know how to profit from it consistently. Click the link here to sign up and test drive to discover the secrets!