The global stock market downturn has been brutal since the Iran-Israel-U.S. conflict broke out. While it has recovered somewhat after the ceasefire, investors are still on the sidelines. However, there is one sector that has gained – oil & gas.

In this article, we detail three oil & gas companies in Malaysia and Singapore that could benefit from high oil prices.

Investment Thesis and Catalyst

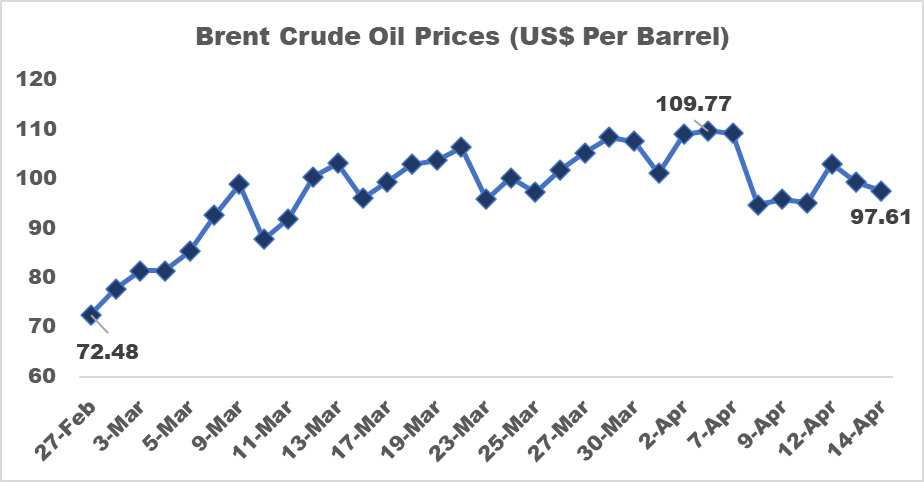

Since the conflict started, Brent crude oil prices have risen to as high as $110 per barrel. Since the ceasefire, it has declined back to about $98 per barrel, but remains higher than pre-conflict levels of about $65 to $75 per barrel.

Source: Investing.com

For oil & gas companies, high oil prices mean they can sell at higher prices. This increases their profit levels and margins.

For example, if an O&G company produces a barrel of crude oil at $40 per barrel, it makes about a 33% gross profit margin ($20 / $60) if it sells at $60 per barrel. However, if prices rise to $100 per barrel, its gross profit margin increases to 60%.

Higher profits from oil & gas companies also provide a boon to companies that provide essential services to the sector, including storage, shipping, logistics and port terminal services.

Hibiscus Petroleum

Hibiscus Petroleum is engaged in the upstream exploration of oil & gas, with assets in Malaysia, the United Kingdom, Australia, Vietnam, and Brunei.

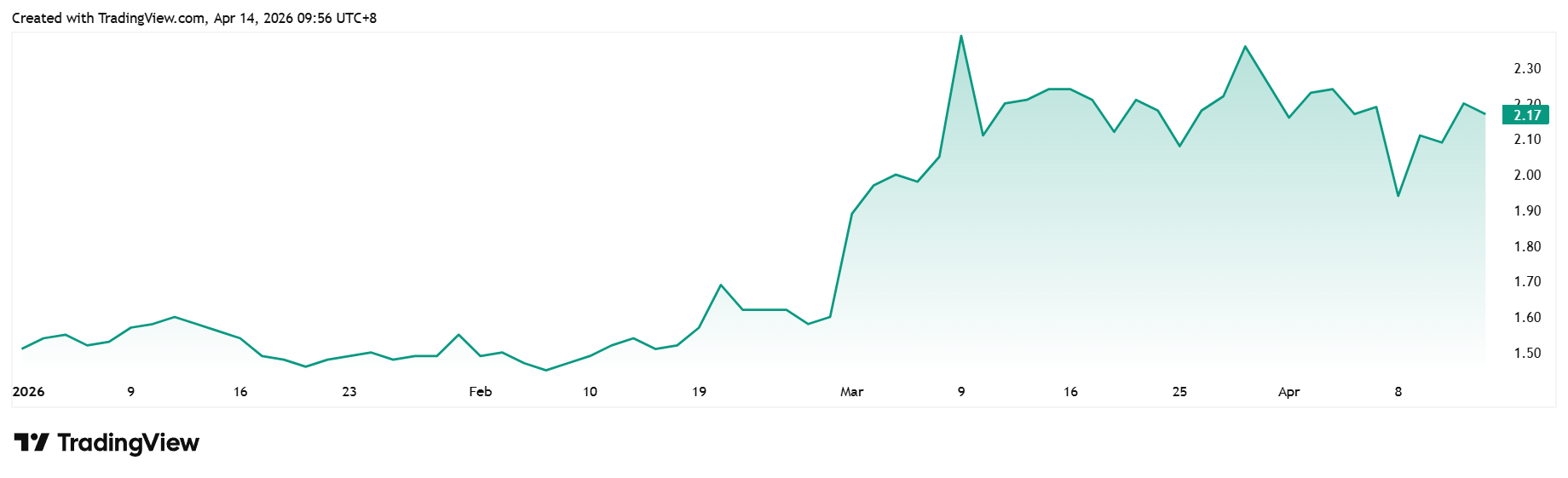

Since the conflict broke out, Hibiscus’s share price has risen from RM1.60 on 27 February to as high as RM2.39 on 9 March. It has since settled at about RM2.16 as of 14 April, up by 35%.

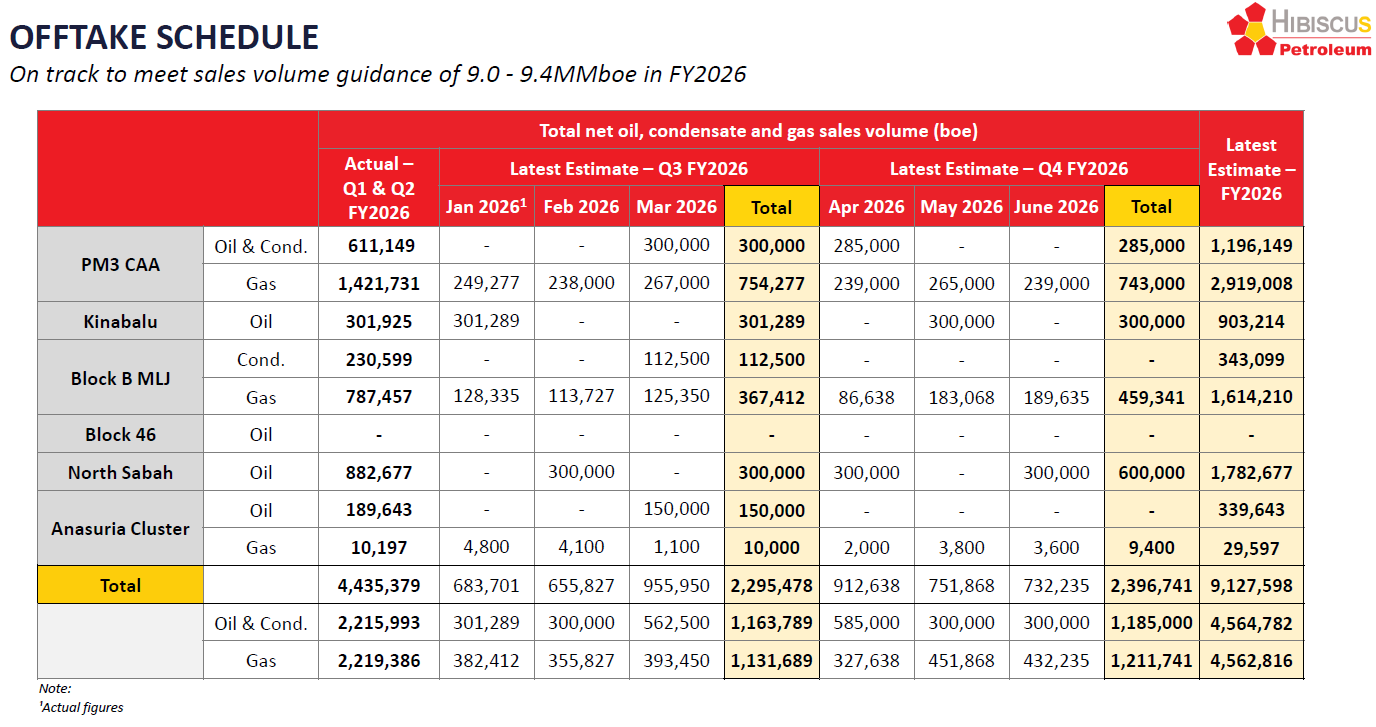

Investors’ interest in Hibiscus is straightforward: an increase in both oil price and production for 2H 2026 (Jan 2026 – June 2026).

- Projected 34% increase in selling price

Average realised oil price (selling price) was US$70.7 per barrel as of 1H 2026 (Jun 2025 – Dec 2025) and could rise to about US$90 to US$95 per barrel for 4Q 2026 (quarter ending 30 June 2026).

- Projected 5.8% increase in production

Based on its production schedule, Hibiscus expects to increase its oil, condensate, and gas production by 5.8% to 4.7 million barrels of oil equivalent (boe) in 2H 2026 from 4.4 million boe in 1H 2026.

Source: Hibiscus 2Q 2026 Report

Financially, Hibiscus Petroleum’s revenue has almost tripled from RM804 million in 2021 to RM2.3 billion in 2025.

- In 2022, it managed to double its revenue to RM1.7 billion as the Russia-Ukraine conflict pushed up crude oil prices to a range of $120 to $130 per barrel.

- However, in 2025, revenue declined by 16% to RM2.3 billion as it also faced low oil prices.

For 2H 2026, investors are expecting a similar situation to the one in 2022. After all, Hibiscus generated its highest profit level of RM652 million and a margin of 38% during that year.

In terms of valuation, Hibiscus is now trading at a relatively high valuation compared to its peers.. Price-to-earnings ratio is 33.1 times compared to its peers’ average of 13.2 times.

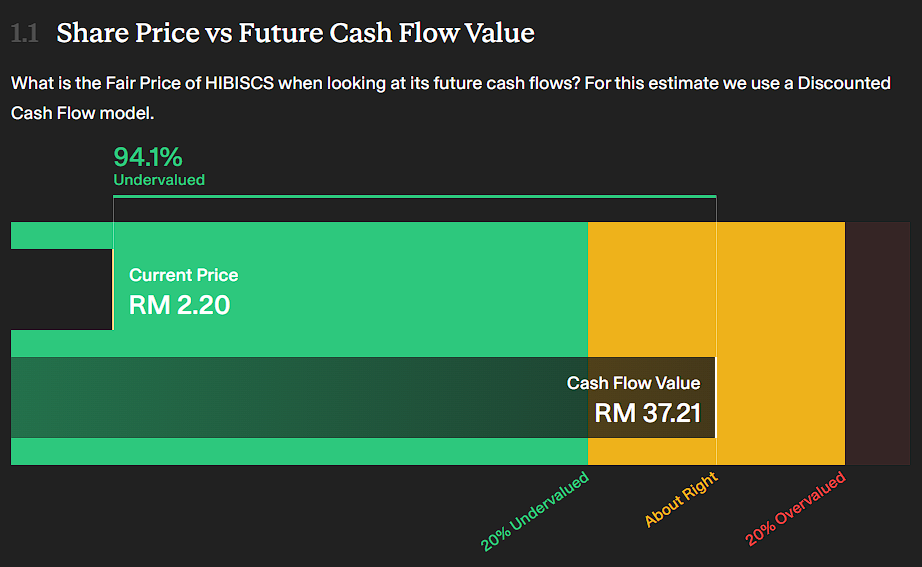

However, according to its discounted cash flow (DCF) valuation, the stock is deemed to be 94.1% undervalued, presenting an attractive entry point.

Source: SimplyWallSt

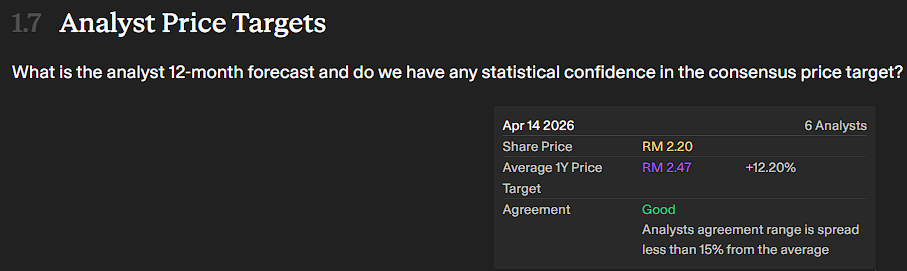

Analysts in the market still think that Hibiscus has legs to run. The target price is set at RM2.47, representing an upside of about +12.2%.

Source: SimplyWallSt

Petronas Chemicals Group

Petronas Chemicals Group (PChem) produces a range of commodity and specialty chemicals for the agriculture, automotive, packaging, personal care, and coatings industries.

PChem has emerged as a prime beneficiary of higher global crude oil and natural gas prices. It uses gas feedstocks as raw materials for its products, sourcing most of them locally in Malaysia (mostly from its parent company, Petronas). It does not rely on gas feedstocks from the Middle East.

This means that PChem is able to keep cost pressures down while also benefiting from higher selling prices. Its competitors, who rely on gas feedstocks from the Middle East, would have to raise prices to protect their profit margins.

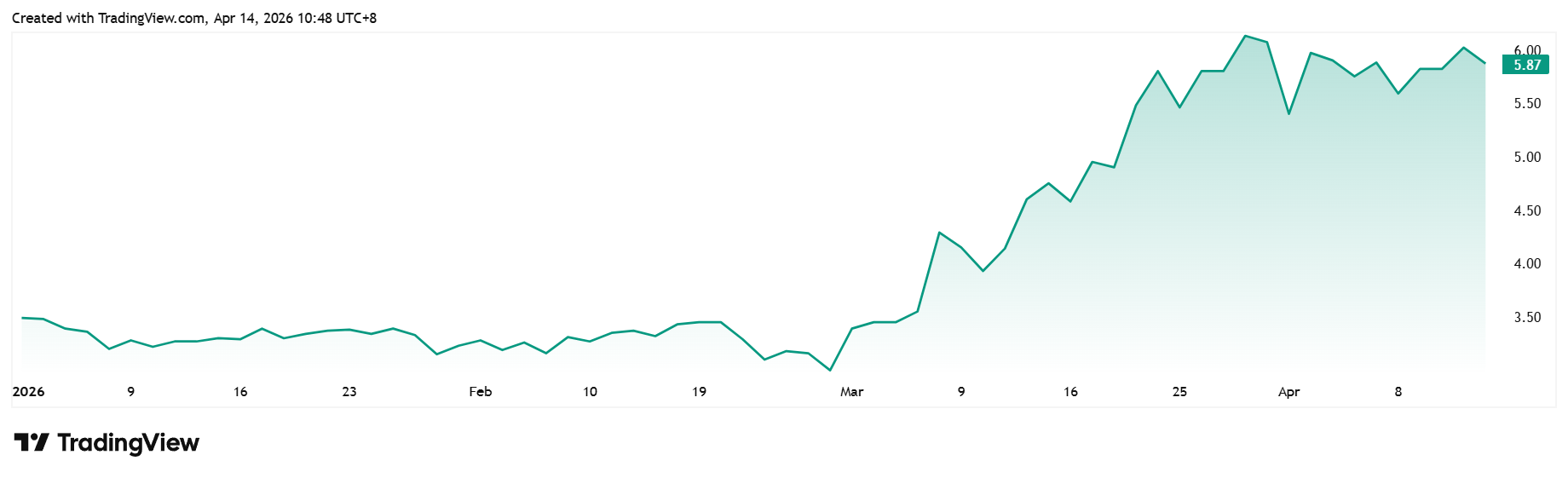

Share price has almost doubled from RM3.00 on 27 Feb to RM5.87 as of 14 April.

This development is positive for PChem as it had a down year in 2025.

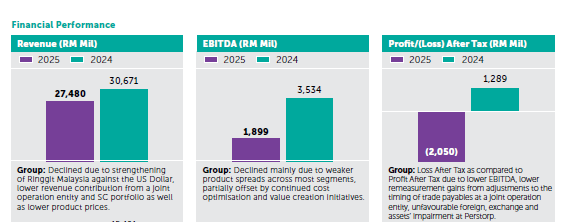

- Revenue was down by 10.4% to RM27.5 billion due to lower selling prices.

- It also suffered a loss of RM2.1 billion compared to a profit of RM1.3 billion in 2024.

Source: PChem Annual Report 2025

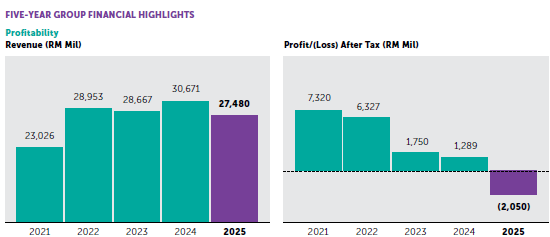

Meanwhile, from a five-year standpoint, PChem could see its revenue and profits recover substantially in 2026.

- Revenue was up by 26% in 2022 when a similar event happened (Russia-Ukraine conflict).

- With higher average selling prices now, net profit margin could improve to about 22%, similar to the one in 2022 (RM6.3 bn / RM29.0 bn = 22%).

Source: PChem Annual Report 2025

PChem regularly pays out about 50% to 80% of its earnings in dividends, providing a stable dividend stream.

However, valuations are now higher than normal due to increased investor interest, which results in a low dividend yield of 1.2%.

RH Petrogas

RH Petrogas (RHP) is an upstream oil & gas player engaged in the exploration and extraction of raw crude oil and natural gas in Southeast Asia. Almost all of its revenue is derived from Indonesia, specifically from the Kepala Burung and Salawati fields.

Let’s not waste time. Several favourable factors are working in favour of Petrogas specifically:

- Higher realised selling prices for 2026 (up to 50% higher)

- Ability to keep cost per barrel low and reap higher profit margins

- Decent oil reserves that can be extracted and sold on demand

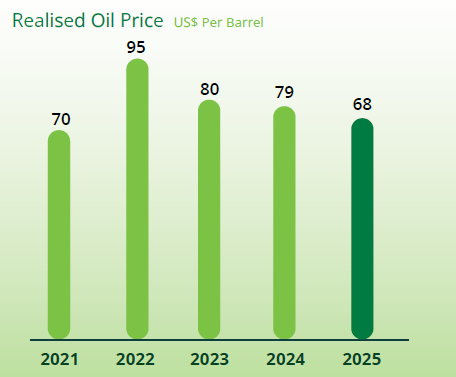

RHP’s realised oil selling price reached its highest of US$95 per barrel in 2022, and has since declined to a low of US$68 per barrel in 2025. With crude oil prices possibly trading higher than US$90 per barrel for the remainder of the year, RHP stands to gain up to 50% higher selling prices.

Source: RH Petrogas 2025 Annual Report

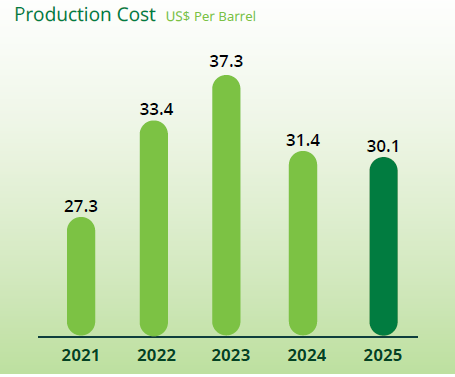

It has also managed to reduce its cost per barrel to US$30 in 2025 from a peak of US$37 in 2023. As production costs tend to be sticky (don’t change much over a period of time), RHP stands to gain a higher profit margin with higher average selling prices.

Source: RH Petrogas 2025 Annual Report

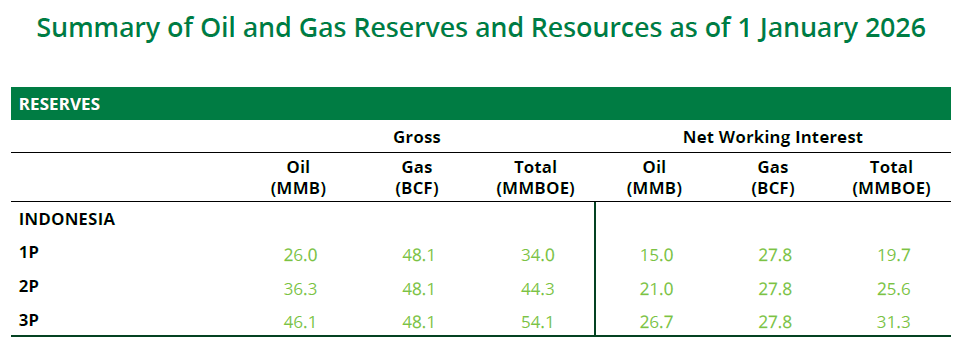

Finally, RHP still has a decent stockpile of oil & gas reserves that it can now sell at higher prices. As of 1 January 2026, it still has about 62.7 million barrels of crude oil that it could theoretically sell. A back-of-the-envelope calculation puts its whole crude oil reserves at US$5.6 billion if they are priced at US$90 per barrel (62.7 million X US$90 per barrel).

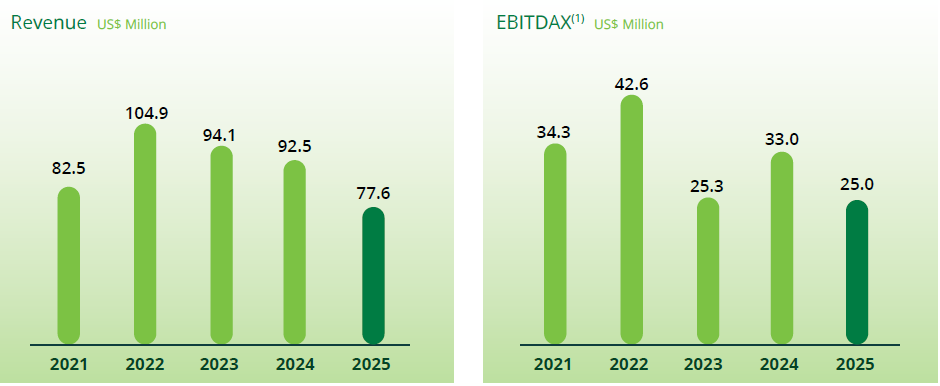

These factors are important for RHP’s prospects in 2026, as it has suffered 3 consecutive years of declining revenue and EBITDA due to lower oil prices.

Source: RH Petrogas 2025 Annual Report

Conclusion

The conflict in the Middle East is uncertain at this point. Even with the ceasefire, the U.S. and Iran have failed to make a deal regarding the Strait of Hormuz.

Oil and gas prices continue to be high for now, and if the conflict persists, these oil & gas stocks could have more legs to run

For investors, the key is to track how investors are moving their funds around. And for now, they are parking their money in the oil & gas sector.

Join our newsletter and unlock access to hidden gems and top dividend stocks and REITs: https://www.smallcapasia.com/#subscribe.