As i am browsing through InvestingNote.com the past week, i noticed an interesting analysis on QAF.

I asked the user “Layers” for permission to share with you and he agreed. So i decided to share with you all too…

Invest in QAF to have free bread supply annually?

QAF is having a bad bad period in their business owing to bad Forex, cynical pork price and divestment of 20% of Gardenia Bakeries (KL) Sdn Bhd. (GBKL)

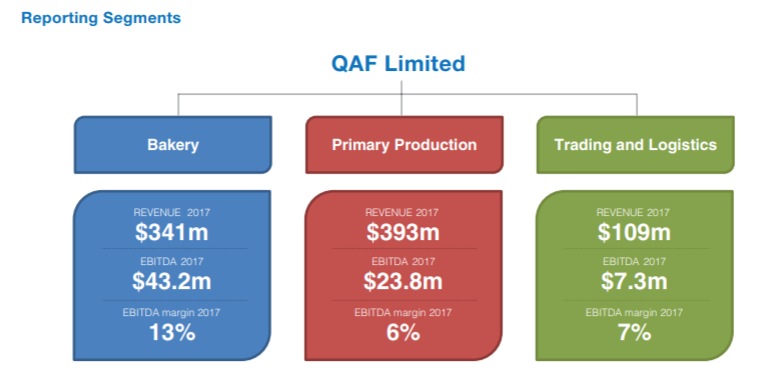

QAF consist of 3 market segments:

- Bakery,

- Primary production and

- Trading & logistic.

For bakery, Gardenia is a top selling brand in Singapore, Malaysia and the Philippines and many other brands. Primary production, Revalea producing pork and animal feeds. Trading & logistic segment is marketed by Ben Foods with brands like farmland.

For bakery, Gardenia is a top selling brand in Singapore, Malaysia and the Philippines and many other brands. Primary production, Revalea producing pork and animal feeds. Trading & logistic segment is marketed by Ben Foods with brands like farmland.

QAF is trying to spin off Primary production, Revalea and focus on the Bakery business. I find this is a good decision.

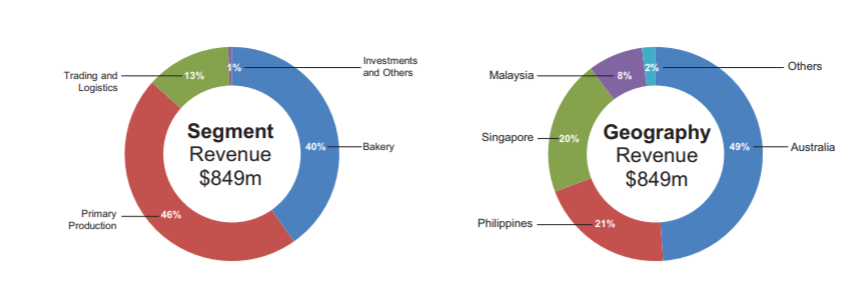

Revalea took up 46% of the group’s revenue yet it has the lowest margin. Focusing on the Bakery segment with 13% EDITDA margin is a better choice.

Wavering Economic Moat

Strong branding and demand for their product across major supermarket and convenient stores. Well this what I like to say but apparently this moat has been weakened probably due to in house brand snatching away the market share.

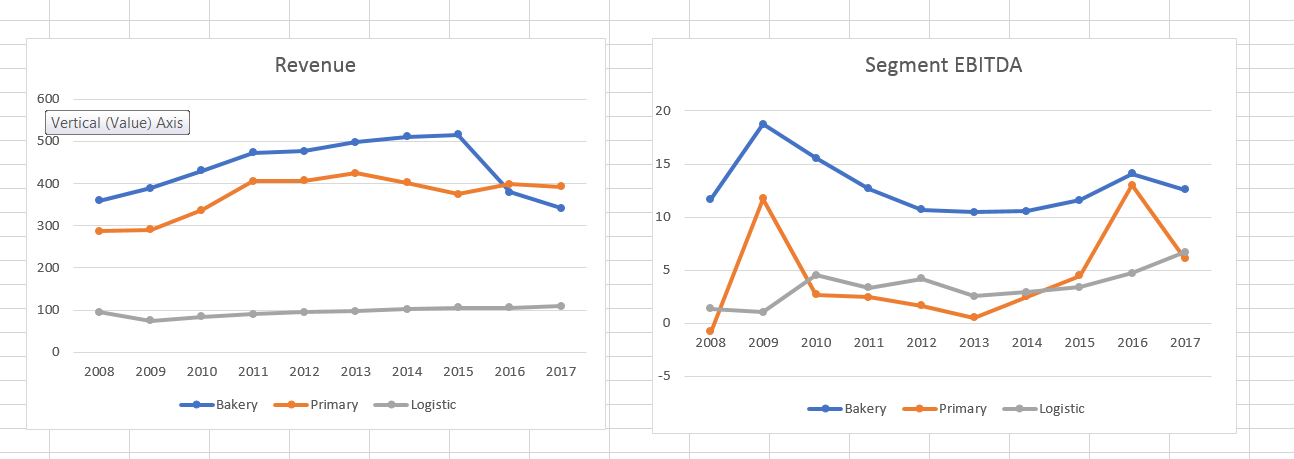

A lot of report has been factoring QAF bad performance to Primary production. However, from the graph below, we can see that bakery did worst in 2016 and 2017, although Primary production has a sharp fall in EBITA. If history is to repeat, Primary production will continue to do badly for a few more years.

QAF to utilize their network effect across different brands and segments

“Going forward, the Group will strive to utilize the strength of each company to grow the food business totally. There will be closer collaborations and potential synergy within the Group will be tapped. For example, a product may be created in a laboratory in one group, made by another, branded by a third group and finally distributed group-wide by all. Ben Foods proprietary products are being distributed in Gardenia’s group network. This has started in the Philippines via 50 franchised Big Smile Bread Station stores and nine Bakers Maison Cafes. Likewise, Gardenia frozen garlic breads and par-baked frozen bread products are sold via the marketing outreach of Ben Foods.”

—- From AR2017

Growth Factor

QAF has 3 more bakery plants to be completed in 2018, 1 in Malaysia and 2 is the Philippines. This will ramp up productions.

Future spin off of Revalea will give QAF more cash to further expand their Bakery segments. Increasing total plant for 12 to 15.

Business Risk

With the plans to spin off Revalea. Growth will be focus on Bakery segment. Looking at the graph, the bakery segment is not doing so well. Ramp up production doesn’t mean more revenue if consumers don’t buy.

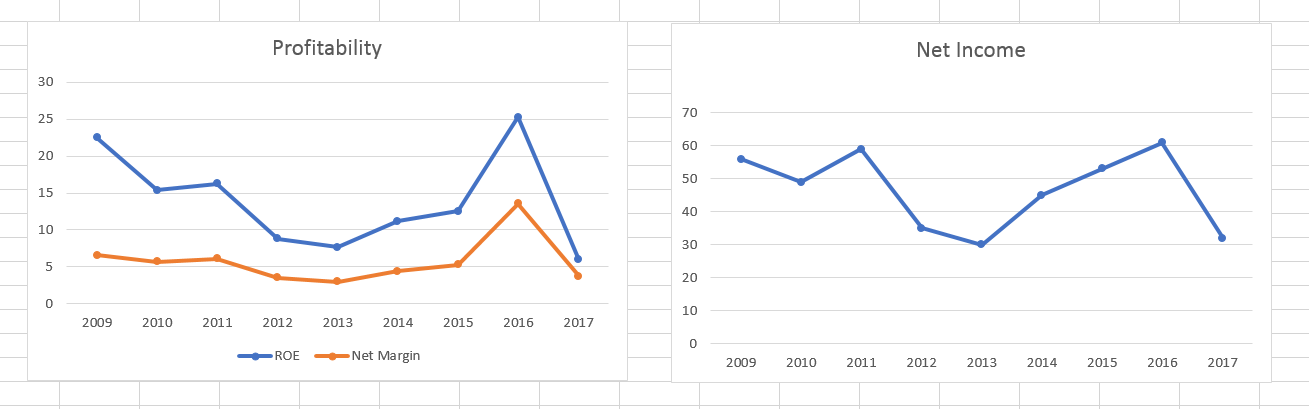

As bakery growth from 2008 to 2015, EBITDA dropped going the opposite direction, probably due to higher expenses. Will QAF manage to grow their bread business well? Profitability is not consistent with Net Profit below 5% most of the time. Net Income seem to going into a down trend over the years.

NOTE: Net income for 2016 exclude one off item from the 20% divestment of GBKL

Conclusion

I do not think this a growth company. Net income is lower than 9 year ago. So far, the annual report talks about ramping up production by building more plants but no concrete plan is being shared.

How about QAF as an income stock? Dividend payout of 5cents out of 5.6 cents seem unsustainable but they need only payout 28million. QAF has cash reserve of 92 million (cash minus current debt). However, a 117 million capex is expected to build the new plants.

In addition if Primary production and bakery continues to drop in 2018, we may see an EPS lower than 5cents.

They finally have a new website.

Not Vested.

This post is contributed by Layers (http://layersinvesting.blogspot.sg/?m=1). Do check out his blog as he shares his thoughts about other companies (Duty Free International, Starhill Global etc.) in details too.