Microsoft Corporation (NASDAQ: MSFT) Statistics:

- Market Cap: $1.056 Trillion(@20-08-2019)

- Price: $138.4(@20-08-2019)

- P/E: 29.72x

- P/B: 10.33x

- Dividend Yield: 1.33%

- Sector: Technology

- Industry: Software

Company Profile:

Microsoft Corporation is an American multinational technology company that develops, manufactures, licenses, supports and sells computer software, consumer electronics, personal computers, and related services.

The word "Microsoft" is a portmanteau of "microcomputer" and "software". Microsoft is ranked No. 30 in the 2018 Fortune 500 rankings of the largest United States corporations by total revenue.

Its best known software products are the Microsoft Windows line of operating systems, the Microsoft Office suite.

Its flagship hardware products are the Xbox video game consoles and the Microsoft Surface line-up of touchscreen personal computers. As of 2016, it is the world's largest software maker by revenue, and one of the world's most valuable companies.

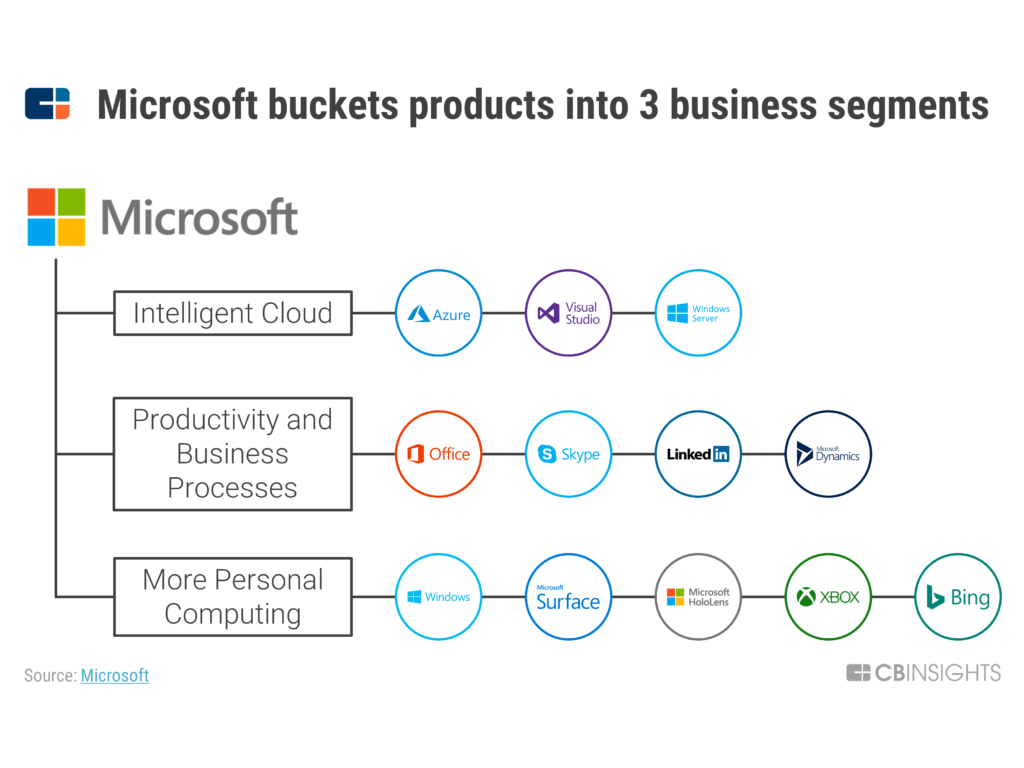

The company is organized into 3 overarching segments:

- Productivity and business processes (legacy Microsoft Office, cloud-based Office 365, Exchange, SharePoint, Skype, LinkedIn, Dynamics),

- Intelligence cloud (infrastructure- and platform-as-a-service offerings Azure, Windows Server OS, SQL Server)

- Personal computing (Windows Client, Xbox, Bing search, display advertising, and Surface laptops, tablets, and desktops).

In 2018, Microsoft surpassed Apple Inc. as the most valuable publicly traded company in the world after being dethroned by the tech giant in 2010 and in April 2019, Microsoft became the third U.S. public company to be valued at over

$1 trillion after Apple and Amazon respectively.

Stock Price Chart

1. Business Model & Economic Moats

As previously mentioned, Microsoft has arranged its business into 3 segments broadly:

-

Productivity and Business Processes

This segment consists of products and services spanning a variety of Applications. This segment primarily comprises:

- Office Commercial, including Office 365 subscriptions and Office licensed on-premises, comprising Office, Exchange, SharePoint, Microsoft Teams, Office 365 Security and Compliance, and Skype for Business, and related Client Access Licenses.

- Office Consumer, including Office 365 subscriptions and Office licensed on-premises, and Office Consumer Services, including Skype, Outlook.com, and OneDrive.

- LinkedIn, including Talent Solutions, Marketing Solutions, and Premium Subscriptions.

- Dynamics business solutions, including Dynamics 365, a set of cloud-based applications across ERP and CRM, Dynamics ERP on-premises, and Dynamics CRM on-premises.

-

Intelligent Cloud

Intelligent Cloud segment consists of public, private, and hybrid server products and cloud services that can power modern business. This segment primarily comprises:

- Server products and cloud services, including SQL Server, Windows Server, Visual Studio, System Center, GitHub, and Azure.

- Enterprise Services, including Premier Support Services and Microsoft Consulting Services.

-

More Personal Computing

More Personal Computing segment consists of products and services geared towards harmonizing the interests of end users, developers, and IT professionals across all devices. This segment primarily comprises:

- Windows, including Windows OEM licensing and other non-volume licensing of the Windows operating system; Windows Commercial, comprising volume licensing of the Windows operating system, Windows cloud services, and other Windows commercial offerings; patent licensing; Windows IoT; and MSN advertising.

- Devices, including Surface, PC accessories, and other intelligent devices.

- Gaming, including Xbox hardware and Xbox software and services, comprising Xbox Live transactions, subscriptions, cloud services, and advertising (“Xbox Live”), video games, and third-party video game royalties.

- Bing Search Engine

Economic moats

Operating System

The key competitive moat that Microsoft carries is the success of the Windows operating system. The Windows OS has penetrated the market to the extent of nearly 90% i.e. 90% of all desktop devices run one or the other Windows OS(almost 1:! ratio of Windows 10 and 7 versions).

The ever successful OS has a lion's share, so much so that, in many localities of Asia and Africa, Windows is considered the only OS in existence. So, it is obvious how much weight the OS alone carries in estimation of competitive advantage.

Cloud Computing

Another front where Microsoft is winning big is its cloud computing business. The company was successful in capturing the opportunity in the next big thing early enough. While Amazon came in as a pioneer in 2006, Microsoft entered the market with "Azure" initially in 2010, the exact time when the segment was turning to the nig thing.

Under the leadership of Satya Nadella, the company developed this segment and after Mr. Nadella was promoted to CEO in 2014, intelligent cloud computing became one of the significant segments. Currently, Azure sports around 22% market share with second place, lagging behind AWS.

Notably, Azure revenue grew 91 percent year-over-year in 2018.

Microsoft Office

Another important product of the company is the Microsoft Office. Office is a software suite consisting of various office application tools such as Powerpoint, Word and Excel. The suite is considered as the gold standard of any "Office" suite and is the first such software bundle available since its first version launched in 1988.

Although the software suffered a minor defeat by Google when they came up with the G-suite (google docs, excel etc); Microsoft has moved the tools to the cloud and offered a subscription service named

Office 365.

From its

website:

Office 365 is a cloud-based subscription service that brings together the best tools for the way people work today. By combining best-in-class apps like Excel and Outlook with powerful cloud services like OneDrive and Microsoft Teams, Office 365 lets anyone create and share anywhere on any device.

Personally, I have heard of various companies adopting this going forward because it combines the many useful tools we use at work into 1 complete package -

- Powerpoint

- Word

- Excel

- Outlook

- Skype for business (messaging software for corporations)

- Microsoft Teams (think #Slack)

- OneDrive (think #Dropbox)

To be honest, i am the most excited about this Office 365 because its a cloud-based subscription service which is going to be the next big recurring revenue driver for the company.

2. Growth Strategy

The company itself has created an elaborate future growth strategy based on their current successes and the visible path ahead:

- "Reinvent productivity and business processes"

- "Build the intelligent cloud platform"

- "Create more personal computing"

- As-a-Service Model

Since, Satya Nadella took over in 2014, the company has changed its strategy from software licensing model to offering all products "as a service".

Windows 10, Office 365, Dynamics 365, Linkedin are all based on

SaaS i.e. software as a service, a subscription based business model. This quantum shift has brought upon the second coming of Microsoft. The legacy that was lost in the Steve Ballmer era was revived, clearly visible in the financials through the years.

Other parts of As-a-Service strategy is IaaS and PaaS which are part of the cloud computing platform Azure. Microsoft offers data storage which is Infrastructure as a service and to compute the data remotely with a vast number of tools on a platform is Platform as a service.

Loosely said, Microsoft has

achieved a 20% growth rate by moving into this business model after years of slump growth.

This behaviour is expected to continue with advantages of the remote computing and ease that comes with it is recognised by the masses unaware.

-

Enterprise Solutions

A big part of the strategy shift was banking on enterprise solutions as the company had achieved peak penetration in the consumer market. The peaking was also visible in the OS business where 90% of devices over the globe was the end.

To do more, Microsoft came into the cloud business following AWS. With Azure, the company was providing a vast number of productivity tools on a single platform.

As we know, Azure may not be a viable option (due to the costs) for an individual consumer using PC but for enterprises, it solved a lot of big issues with in-house servers, and multiple third-party softwares for management and planning.

Similar cloud based solutions were brought to enterprise with Office 365 and Dynamic 365. Office 365 offers productive tools for businesses on a SaaS model as said earlier.

On the other hand, Dynamic 365 is a major platform for enterprise resource planning(ERP) and customer relationship management(CRM). Both products have significant market share and the required potential to capture more.

Other products for developer enterprises such as Visual Studio and GitHub have also witnessed major growth.

-

Consumer End

A major win in the consumer front comes with the gaming business. For a long time, Xbox is Microsoft's flagship gaming console going up against Ninetendo Wii and Sony Playstation.

However, as Google has unveiled Stadia, dubbed as "the Netflix of gaming"; Microsoft is not resting on its laurels too.

They are in the pipeline of launching their own subscription based gaming service

xCloud to also counter online game platforms like Steam, Playstation One and Google's similar project.

A hint of the future in consumer devices is the smaller acquisitions in virtual reality and artificial intelligence in addition to the major acquisition in Mixed Reality based devices "Hololens".

3. Financial Analysis

The qualitative data doesn't mean much without the numbers showing the proof. Let's look at the financial numbers now:

(i) Financial Performance

For a trillion dollar company, Microsoft is growing at a great pace with excellent top and bottomline numbers.

Based on the blue bar (revenue), Microsoft has doubled its revenue from FY2010 to FY2019 - translating into an annual compounded growth rate of 7%.

However, if you look at FY2018 and FY2019, revenue is starting to deliver double-digit growth despite of a higher revenue base.

And looking at the above, profit attributable to shareholders jumped 136% on a year-to-year basis to US39.2 billion.

If you look at their

FY2019 press release, CEO Satya Nadella commented:

“It was a record fiscal year for Microsoft, a result of our deep partnerships with leading companies in every industry.

Every day we work alongside our customers to help them build their own digital capability - innovating with them, creating new businesses with them, and earning their trust.

This commitment to our customers’ success is resulting in larger, multi-year commercial cloud agreements and growing momentum across every layer of our technology stack.”

To further add on, we went to check out the financial ratios of Microsoft and we are amazed.

FY2015 shows a ROE of 14.4% and ROIC of 11.1% and net margins of 13.03%.

Fast forward to FY2019, the company sports a ROE of 14.4% and ROIC of 24.1% and net margins of 31.2%. Talk about management efficiency!

This is testament to their growth strategy Microsoft has implemented - and we are sanguine that it will continue to pan out.

(ii) Balance Sheet + Cash Flow Position

With all the free cashflow rolling in due to their asset-light business model, Microsoft Corp has a rock solid financial position.

Their cash hoard amounts to a whooping USD 133.8 billion with only USD 78.4 billion of total debt. It means they can pay off the debt anytime!

We also like the increase in their operating cash flow and free cash flow over the past 3 years.

Financial Health Summary:

With the above figures, Microsoft Corp has nothing to worry about even if a recession hits.

4. Management Team Assessment

A chart of all key management with their respective roles in the company.

Satya Nadella

Mr. Nadella has been key to the resumption of excellent business at Microsoft. Before being named CEO in February 2014, Nadella held leadership roles in both enterprise and consumer businesses across the company.

Joining Microsoft in 1992, he quickly became known as a leader who could span a breadth of technologies and businesses to transform some of Microsoft’s biggest product offerings.

Most recently, Nadella was executive vice president of Microsoft’s Cloud and Enterprise group. In this role he led the transformation to the cloud infrastructure and services business, which outperformed the market and took share from competition. Previously, Nadella led R&D for the Online Services Division and was vice president of the Microsoft Business Division. Before joining Microsoft, Nadella was a member of the technology staff at Sun Microsystems.

Originally from Hyderabad, India, Nadella earned a bachelor’s degree in electrical engineering from Mangalore University, a master’s degree in computer science from the University of Wisconsin – Milwaukee and a master’s degree in business administration from the University of Chicago.

Compensation Levels

Source: Salary.com

For a giant like Microsoft, the executive compensation is very fair and a big portion is paid in equity too. Even the CEO Satya Nadella is payed US$25.8 million in total - that's only 0.06% of their net income (not even revenue!).

There is no exuberance to be found in the compensation of key executives which quite the opposite of tech company. This is an indicator of prudence and candour in the management and its vision.

It also aligns the interests of the top management to that of the shareholders.

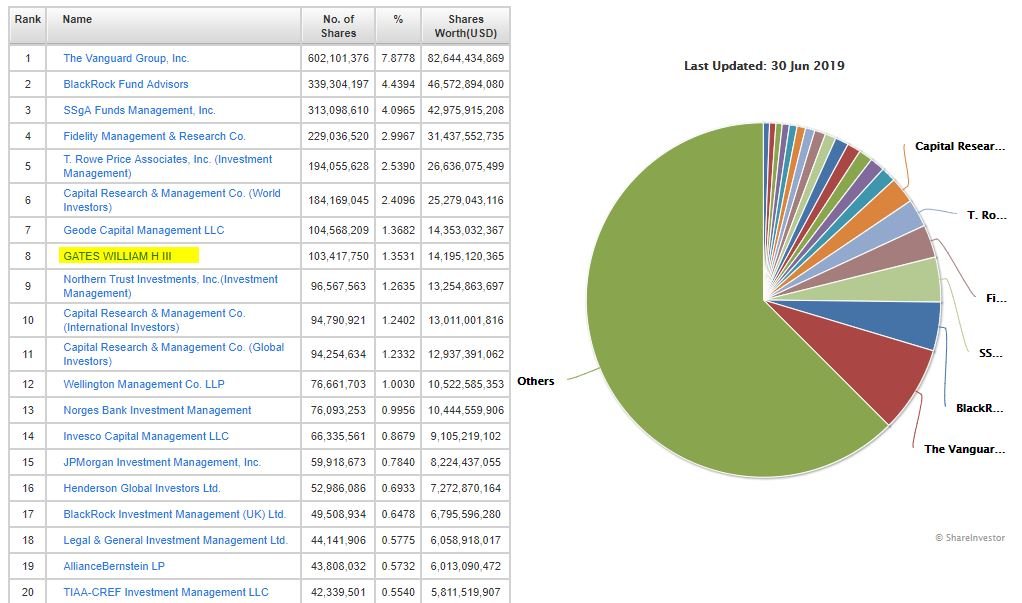

Shareholding Structure

In the post success era of a tech company, Microsoft shareholding is full of institutional investors. The founder Bill Gates still holds about 1.35% stake in the trillion dollar giant.

As mentioned, the top management is compensated in equity and options but that is miniscule in its order of millions of dollars.

For the most shareholder record of Microsoft is not of the significance because of active institutional holders and the shear reputation that the company holds overall.

Source: Shareinvestor.com

5. Risks

(i) Fights at multiple fronts

Microsoft Corp, being the behemoth it is, is not risk-proof where you can just sit around being complacent. The main reason is the constant change in new breakthrough technology and consumer behaviour.

And Microsoft is constantly up against many big tech companies as well i.e. Google, Apple, Amazon or Oracle etc.

We have come up with a sample list of competitors in the major segments of Microsoft:

- Operating System: Windows vs MacOS, ChromeOS, Linux.

- Cloud Computing: Azure vs AWS, Google cloud, Alibaba cloud, SAP, HP, Dell VMWare etc

- Productivity tools: Office 365, Dynamic 365 vs Salesforce.com, G suite, Oracle, Adobe, Zoho etc.

- Gaming: Xbox vs Playstation, Nintendo, WII, Steam etc.

- Extended reality tech: Hololens vs Google Glass, Magic Leap, Oculus etc

As you can see, competition is stiff in the tech world and it is almost impossible to know beforehand on who or what will succeed eventually.

Even the big names like IBM and Xerox have been defeated by then underdogs in several markets, so no reason to think that can't happen with Microsoft.

Conclusion

First of all, lets start off with how much Microsoft Corporation is worth. We derive an intrinsic value of US$150.13 based on the following assumptions:

- Annual 12.25% EPS growth for next 10 years (taken from packaged software industry past 5 years' growth rate)

- Discount rate of 10% (a good number for public SAAS companies based on https://www.forentrepreneurs.com/discount-rate-for-dcf/)

- Terminal growth rate of 3%*

*Terminal growth rate represents an assumption that the company will continue to grow (or decline) at a steady, constant rate into perpetuity. The perpetuity growth rates range between the historical inflation rate of 2 - 3% and the historical GDP growth rate of 4 - 5%. Thus, we set it as 3% because we think Microsoft Corp is a great company which can continue to grow on par with inflation.

In short, Microsoft Corporation is trading at around fair value at its current share price of US$133.39.

That said, we like how Microsoft has turned itself into a cloud company successfully. No longer the old-rigid company of the past, it has developed the agility and presence of mind to take it to the trillion dollar valuation mark.

Furthermore, we feel that there is still a huge TAM (total addressable market) for its new products (LinkedIn, Office 365, Azure cloud, Xcloud etc). The pristine financial position and consistent free cash flow are great 'bonuses' to have as well.

To conclude, Microsoft checks all our boxes for being a great growth company. Although it is already a Trillion dollar company, we have no doubt that it can increase to be even a 2-trillion or 3-trillion market cap if the stars are aligned while Microsoft continues to compound on its success.

For more information, you can check out the links below:

https://view.officeapps.live.com/op/view.aspx?src=https://c.s-microsoft.com/en-us/CMSFiles/SlidesFY19Q4.pptx?version=57904466-7e87-bcd6-1a59-9e4c5e26a761

https://view.officeapps.live.com/op/view.aspx?src=https://c.s-microsoft.com/en-us/CMSFiles/TranscriptFY19Q4.docx?version=21b560a7-8457-c458-b565-816bc71cc9ad

https://venturebeat.com/2019/07/18/microsoft-earnings-q4-2019/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}