Looking for a trusted Stock Remisier?

Augustine works closely with a small group of clients - providing regular market updates, Bazi & astrology wealth insights, and clear guidance to invest with confidence.

📩 Check out my profile here today!

Keppel DC REIT (KDC) invest in a portfolio of income-producing real estate assets which are used primarily for data centre purposes, as well as real estate and assets necessary to support the digital economy.

The REIT has an AUM of $3.7b with 23 data centres spread across 9 countries as at 31 Dec 2022.

The REIT posted an excellent set of results for the full year ended 31 Dec 2022.

Lets dive deeper into the results and why there are 4 reasons you could be excited about KDC REIT.

1. Key Financial Metrics

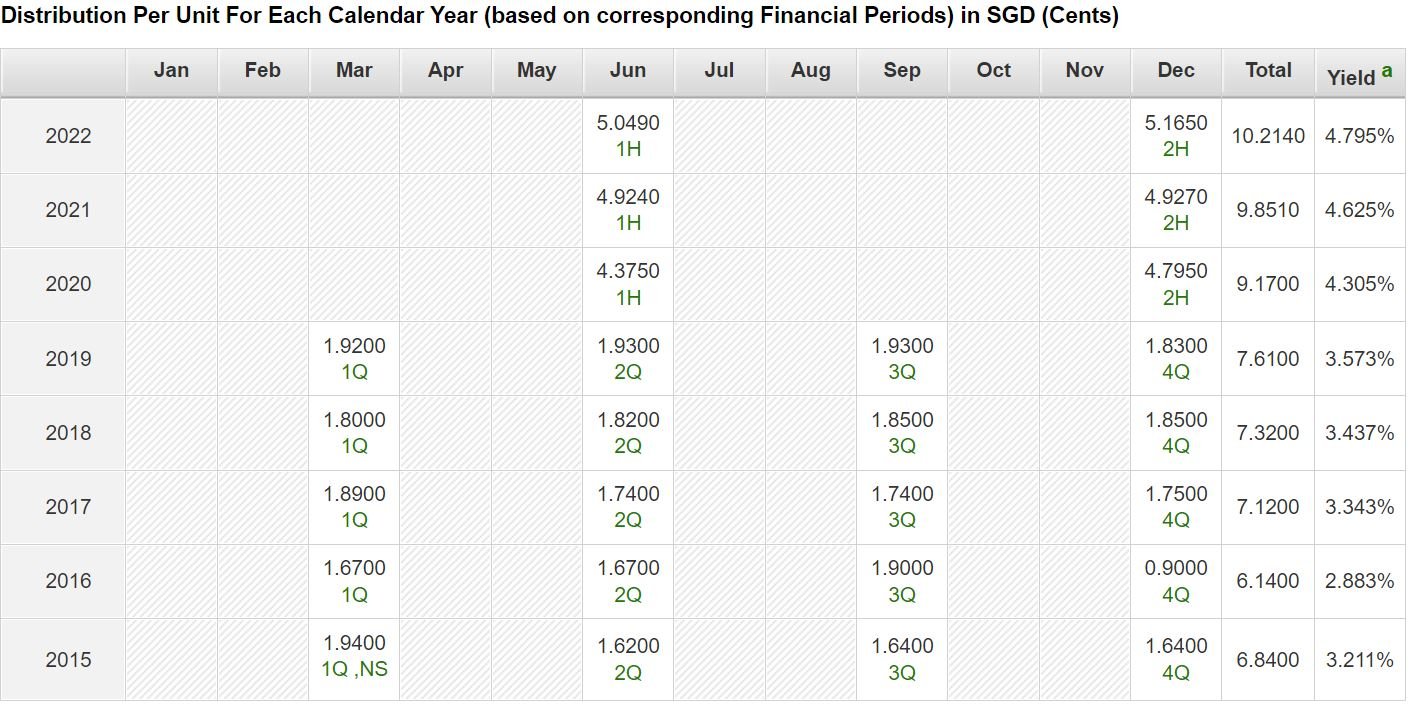

The REIT reported an increase of 7.7% in distributable income to $184.9 million while DPU increase by 3.7% to 10.214 cents. The REIT strengthened its portfolio occupancy from 98.3% as at end-2021 to 98.5%1 as at end-2022.

Its WALE has been lengthen from 7.5 years as at end-2021 to 8.4 years as at end-2022. This will enable the REIT to have stable distributions for unit holders.

There is also continued leasing momentum with healthy renewals and expansion by existing clients.

It has built-in income and rental escalations based on CPI or similar indexation, or fixed rate mechanisms embedded in more than 50% of the portfolio. This will also help to mitigate impact of inflation and rising energy costs.

2. Healthy Balance Sheet

KDC aggregate leverage is relatively healthy at 36.4% while cost of debt remains low at 2.2%. It also has a high interest coverage of 7.6 times.

The REIT only has about 11% of their debt maturing in FY 2023 which will enable them to mitigate the impact of rising interest rates and finance costs.

3. Potential Acqusitions

As a pure-play data centre REIT, the REIT’s future growth is dependent on the continued demand for quality data centres.

The world’s data needs continue to grow exponentially, while the growth in key data centre hubs continues to be limited by power and land availability.

Worldwide co-location market continues to expand at a double-digit growth rate (2022 estimate: 14%, 2023 estimate: 15%), with hyper-scalers accounting for the bulk of the growth.

With the backing of its sponsor Keppel, Keppel DC REIT potential data centre assets for acquisitions amount to over $2 Billion mainly through Keppel T&T and Keppel’s private data centre funds.

Some of Keppel DC's potential target markets are Canada, France, Hong Kong, Indonesia, etc.

4. Valuation

The Singapore 10 yield bond yield has been increasing in 2021 and reached 3.57% recently - its highest since 2017.

Although it has since dropped to 2.92%, the rising risk free rate has make REITs less attractive causing a more than 14% decline in the REIT index in 2022.

Keppel DC REIT was no exception. Its share price has fallen from a peak of ~3.00 in October 2020 to $1.79 by end of 2022 - representing a decline of 40%!

Keppel DC REIT review after its drop

The question on many people's minds is this:

"Is Keppel DC still attractive at current price level?"

Keppel DC yield ranges from 3.21% in 2015 to the current 4.79%. Although, Its share price has since gained 19% year to date, Keppel DC REIT still looks attractive at current prices based on the yield difference of its current yield versus the historical average yield.

However, if inflation remains sticky and thus interest rates will have to remain high, will other higher yield REITs be more attractive than Keppel DC REIT?

Subscribe to our newsletter for more updates on Keppel DC REIT as the year unfolds.

You can view KDC REIT website

here.

Be A Valued Client of Augustine in Lim&Tan Securities

Receive Augustine’s regular stock updates via Telegram plus full access to his private client hub with exclusive research, astrology and Bazi insights.

(Exclusive Readings for Clients Only)

{kind=link}