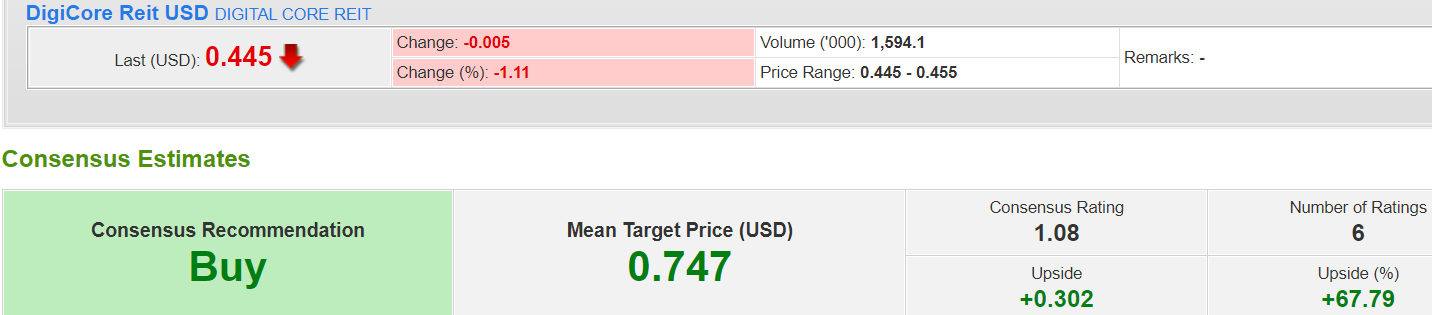

#2 Digicore REIT USD

Digicore REIT currently has an upside potential of 67.8% based on the average of 6 analysts.

Digicore is a real estate investment trust which invests in data centres-related assets globally. It currently has USD1.6 billion of assets under management consisting of 11 data centres in U.S., Canada, and Germany, with 98% of its spaces occupied.

As Digicore was just listed in 2021, only financial numbers for full year 2022 were available. Digicore 's revenue came in at USD115 million and it registered a net profit of USD7 million.

Similar to ManuLife, Digicore 's properties' value declined by USD29 million over the year due to the Fed's interest rate hikes but these losses were only on paper. From its operating cash flows, Dcore generated USD78 million in cash.

In terms of valuation, Digicore is currently trading at a lower price-to-book ratio of 0.54 times compared to the peers average of 0.94 times.

Digicore could be a good investment to consider for the following reasons:

- The expected stop in Federal Reserve raising interest rates this year will be positive to the property market.

- Steady dividend yields of 4.9%, quite high for a data centre REIT.

- Increase in demand for digital economy-related services = Increased demand for data centres in long run.

#3 Food Empire

Analysts are targeting for a price of SGD1.31 for Food Empire (FE) compared to the current share price of SGD1.01. This implies a potential upside of 29.8%, despite the share price going up pretty sharply.

FE is a food and beverage company that produces and sells instant beverage, frozen convenience food and confectionary products to over 50 countries in the world. Notable brands include MacCoffee, CafePho, Klassno, and Petroskaya Sloboda.

You will be glad to know that FE's financial performance has grown to its highest level in 2022. Profits in particular tripled from SGD26 million in 2021 to SGD81 million in 2022. Meanwhile, revenue grew by 23.6% to SGD536 million in 2022.

In terms of valuation, FE is trading at a low price-to-earning ratio of 6.36x compared to the industry average of 17.69 times.

Hence, you could take a good look at FE for the following reasons:

- Strong growth in revenue during the pandemic. It grew by 48% from 2020 to 2022.

- The Russia war was a blessing in disguise for the firm because coffee demand actually went up!

- India's freeze-dried factory and Vietnam's demand are the twin growth engines today...

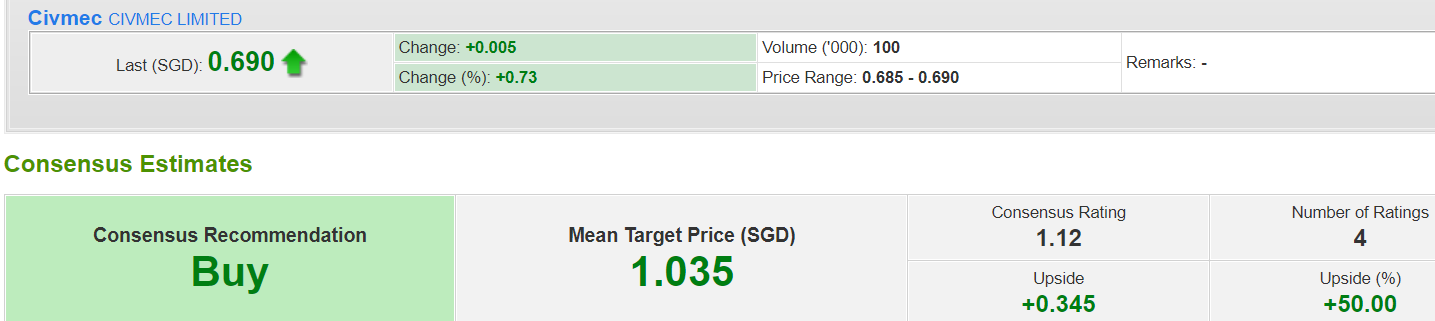

#4 Civmec Limited

Civmec Limited (CML) has an upside potential of ~50% with a price of SGD1.04 compared to the current share price of SGD0.69.

CML is based in Australia and provides construction and heavy engineering services to the oil & gas, mining, infrastructure, utilities, chemical, and power industries.

CML is finally back to its pre-pandemic financial performance. Revenue has recovered SGD776 million in 2022 compared to SGD739 million in 2019.

The good news is that profits are actually much higher at SGD48.7 million compared to SGD5.8 million over the same period.

When it comes to CML's valuation, it is currently trading at a low price-to-earnings ratio of 6.6x compared to the industrial average of 13.1x.

Hence, CML could be worth taking a good look at for the following reasons:

- Cyclical at low valuations.

- Easing of coal export ban by China - a positive sign for Australia's mining industry (Civmec customers).

- High return on assets of 8.3% compared to the industry average of 3.4%.

CML's dividend yield of 4.4% in 2022 is higher than its historical average of about 1% to 2%, making this an attractive investment to hold for dividends.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}