#2 AIMS APAC REIT

AIMS APAC REIT's (AA REIT) Chairman, George Wang's deemed interest in AIMS increased from 9.8% to 10.4% as 4.7 million shares were issued as payment for management fees.

AA REIT is a real estate investment trust that buys and manages logistics, warehouses, business parks, and industrial and high-tech spaces in Singapore and Australia.

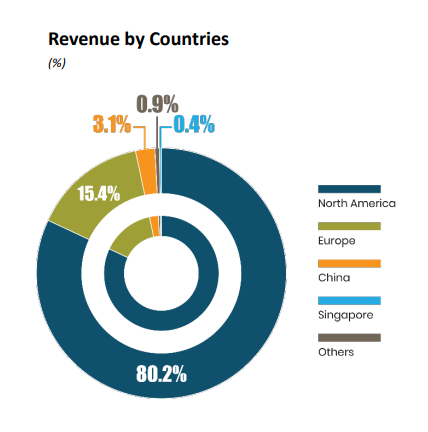

It has 26 and 3 properties in Singapore and Australia respectively, while managing S$2.3 billion in assets. Properties in Singapore generate the bulk of AA REIT's revenue at 90%.

In terms of financial performance, AA REIT has remained resilient even throughout the pandemic years and high interest rates in 2022.

Revenue grew by 17.6% to S$167 million in 2023 (Mar 2022 - Mar 2023) from S$142 million in 2022 and was driven mainly by new acquisitions and higher rental from its logistics, warehouse, high-tech, and industrial properties.

With AA REIT's tenants focused on the trade-oriented sectors in Singapore, 2022 has been a good year.

Total merchandise trade in Singapore continued to register double-digit growth of 17.7% in 2022 compared to 19.7% in 2021.

While 2023 is expected to be a down year for global trade, 2024 is expected to be a year of recovery as most economies around the world start to recover from the high-interest rate environment.

AA REIT currently has a BUY recommendation from analysts with an average target price of S$1.55.

This implies a total upside of 24.9%, with capital gains upside of 17.4% and current

dividend yield of 7.5%.

#3 CapLand China T

Similar to CapLand India T, Temasek's deemed interest in CapLand China T (CapChina) increased to 31.1% from 30.5% previously amid the payment of management fees in CapChina's stocks to Temasek's subsidiaries.

CapChina is a real estate investment trust focused on investing in shopping malls, business and logistics parks in China. It currently manages around S$5.2 billion in assets.

Its retail portfolio (shopping malls) is the biggest at 69% of its assets, followed by business parks (26%) and logistics parks (5%).

The occupancy rate for its retail portfolio is also the highest at 96.4%.

In 2022, CapChina has weathered the severe lockdown restrictions in China quite well.

After revenue rebounded by 79.5% in 2021, it further grew by 1.4% to S$383 million in 2022 from S$378 million in 2021, boosted by higher rentals for business and logistics parks.

In line with the reopening of China's economy in 2023, the following factors could be the factors Temasek is not disposing of the additional shares that have been issued to its subsidiaries

- Strong Retail Sales Recovery in China

Retail sales grew by double digits in March and April 2023 at 10.6% and 18.4% respectively as Chinese consumption appetite recovers from the lockdown restrictions in 2022.

- Steady Industrial Production Recovery in China

Industrial production growth continued to rise to 5.6% in April 2023 from 3.9% in March 2023.

Most analysts in the market have an OVERWEIGHT call on CapChina and an average target price of S$1.30.

This implies a total upside of 29.7%, with a capital gains upside of 23% and a current

dividend yield of 6.7%.

#4 Aztech Global

Yew Mun Hong, Aztech Global's (AG) Chief Executive Officer increased his stake slightly to 70.3% from 70.2% previously on 16 May 2023.

AG provides one-stop design and manufacturing services for products such as Internet-of-Thing (IoT), data communication, and LED lighting.

It currently has 4 research and development centers in Singapore, Hong Kong, and China and 3 manufacturing facilities in Malaysia and China.

Most of AG's revenue is derived from the United States, encompassing about 80%, followed by Europe (15%) and China (3%).

AG has been very impressive in its financial performance.

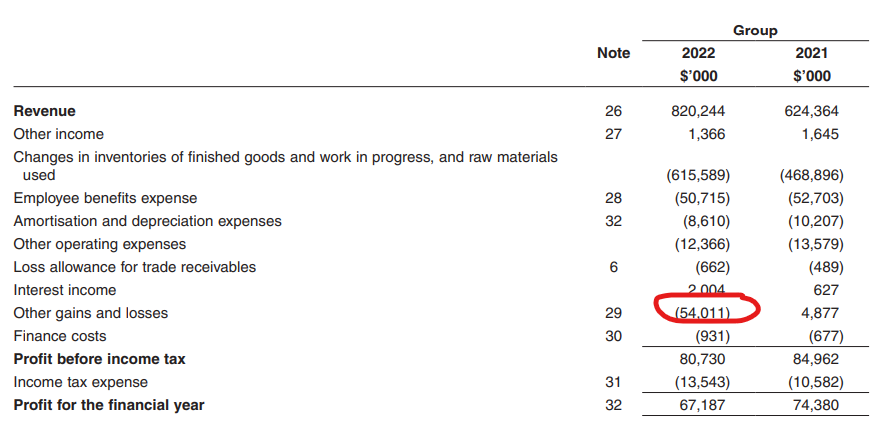

Revenue almost doubled from S$484 million in 2020 to S$820 million in 2022, and this was driven mainly by its IoT and data communications divisions.

However, its net profits declined from S$74 million in 2021 to S$67 million in 2022, due to foreign exchange loss that is recognised as it is not used for hedging purposes.

Hence, on an operating cash flow basis, cash from operations more than doubled to S$106 million in 2022 from S$42 million in 2021.

AG's CEO might be confident in AG's prospects due to the following reasons:

- Possibly higher demand from the U.S. as interest rate hikes reach the end.

Many market investors are expecting that the Fed's interest rate hikes have reached an end in May 2023, and the Fed could reduce interest rates moving forward. This will be supportive of demand from the U.S.

- IoT global market projected to grow at a strong rate

The global IoT market is expected to grow at a 6.7% average growth rate from US$88.2 billion in 2023 to US$106.1 billion in 2026.

Most market analysts have AG at a BUY investment call and an average target price of S$0.99.

This implies a total upside of 50%, with a capital gains upside of 44.8% and a current

dividend yield of 5.2%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}